1 The US bond market

2 Europe

3 Russia

4 Iran

Introduction

With the fall of the Soviet Union, the world was going to become a better place- according to the Rockefeller family. Just over 3 decades later, the celebratory mood looks positively deluded. The end of the Cold War brought not a peace dividend. Rather it unleashed an epidemic of greed. With the fear of mutually assured destruction behind it, the Rockefeller Empire unveiled a new doctrine: “full-spectrum global dominance”, militarily and economically. The ideological war between the West and Communism came to an end. Global contests would take place in the economic field. It has a physical form too. Giant corporations that seek monopolistic control over other countries’ resources. And a gargantuan war machine headquartered in the US, but with 800 bases around the globe, that is ready to crush those who stand in the way of ever-greater wealth accumulation by a tiny elite. The 2 families are never satiated. They are driven to constantly entrench and expand their control, to amass more wealth, to buy more influence in our pretend-democracies, to be more ruthless against anyone or anything that threatens their dominance. Capitalism without constraints would produce resistance. War and profit are intimately tied together. War drums sound ever more loudly across the globe. Ask Venezuelans, Cubans, Greenlanders, Ukrainians, Russians, Palestinians, Lebanese, Iranians how the grab for global dominance is working out for them. Ask Europeans and Americans too, now permanently mired in the politics of austerity. Ever more workers have been forced into the gig economy, with zero-hours contracts. And that is before an AI “revolution” makes swathes of jobs redundant.

1 The US Bond Market

From the early 1960s, Wall Street exported inflation to the rest of the world by refusing to devalue the dollar. When the world rose up against this policy by cashing in its dollar holdings for gold, the Rockefeller Empire cancelled the “gold-window” at the Fed. It took a war (Oct 1973) and a global energy crisis before the Petro-dollar was established. Since then, the US increased the amount of inflation it exported to the globe, through various economic, financial and trade policies. This helped to keep prices extremely low for the American consumers- who kept on chasing the “American Dream “- a brilliant con job. Now, the tide is turning. DE-dollarization is hurting the US and EU economies. As economies around the world reduce the usage of dollars, these unwanted dollars return back to the US. As more money chases the same amount of goods, prices rise. Then came Covid, Ukraine, Gaza and Iran- all of which have brought about broken supply chains, higher energy and food prices. The resulting inflation is forcing interest rates to rise. This, in turn is hammering US bond prices downwards. And, here lies a brewing problem. As inflation rises in the West, central banks are raising interest rates to crush this. As interest rates rise, bond values fall. The fall in values is upsetting foreign bond holders. Secondly, rising interest rates on Wall Street is attracting huge flows into the dollar- earning 5 % is better than earning 1% (Japan) or 2% in Euro-bonds. This, in turn, is weakening the currencies of many large exporters such as China, Japan and South Korea. In order to defend their currencies, many are selling their US Treasury bonds, and using it to strengthen their own currency, in order to reduce cost of imports and still be competitive on its exports. Within the West, its citizens enjoyed a high standard of life. But this was possible only because of unequal terms of trade, finance and economics. This attracted millions of people to pour into these two zones. Who doesn’t want a better quality of life? The West exported its inflation to the Global South. As paper money fades to be replaced by a physical economy, we find that this has created inflation in the West. Inflation in the US was rising, but slowly. After Covid and broken supply chains, inflation increased. Then came the Ukraine war and attacks and boycotts on Russian energy. Inflation increased further. And then the attack on Iran. A huge loss of energy and other goods. Inflation is now turbo-charged. Raging inflation, loss of jobs and a declining standard of living is now producing the American Nightmare. As George Carlin once said, “That’s why they call it the American Dream, because you have to be asleep to believe it “. That’s one problem. The next one is next – – –

The UAE’s $95 Billion Problem: Why a Rich Nation Begged Washington for Cash

Let me tell you something that sounds absurd on the surface. The United Arab Emirates just walked into the U.S. Treasury with its hat in hand, asking for an emergency loan. Now, if you know anything about the UAE, your first reaction is probably laughter. This is a country that parks its sports cars in the desert for fun. It sits on roughly $114 billion in U.S. Treasury bonds as of March 2026, hundreds of billions more in foreign exchange reserves, and has sovereign wealth funds that could buy small European nations before lunch. So what gives? Why would a nation swimming in wealth suddenly need a lifeline? Here is the thing nobody on Wall Street wants to admit out loud. The UAE is not broke. Not even close. But it is trapped in a financial chokehold that has nothing to do with how much money it owns and everything to do with what it would have to destroy to access that money. Ther’s a ticking bomb in the U.S. Treasury market that most analysts are sleepwalking past. This vulnerability will define every trading floor conversation for the next few years. Let me walk you through why the richest kid in the room just became the canary in the coal mine. The mechanism is almost insultingly simple. Washington spends trillions more than it collects every single year. To cover the gap, it sells IOUs called Treasury bonds to anyone willing to buy them. For decades, this was the greatest financial arrangement in history. Foreign governments parked their savings in these bonds because they were safe, liquid, and denominated in dollars. But here is where it gets ugly. As a nation whose primary export is oil, when a war shuts down your oil exports, and you suddenly need hard currency, that’s cash flow in the economy, to keep the lights on, you do not sell your palaces or your airline. You sell the most liquid dollar asset you own. You dump Treasuries. And when enough countries do that simultaneously, the price of those bonds’ collapses. When bond prices fall, yields spike. And because Treasury yields anchor every borrowing cost in America and the world, from your mortgage to the government deficit, the entire economy feels the whiplash. So, picture the UAE’s predicament. The Strait of Hormuz has been effectively closed for 15 weeks. Oil revenues, which fund the kingdom’s everything, have dried up. The UAE needs dollars immediately to pay bills, buy fuel, and keep its economy from seizing. It could sell its $114 billion in Treasuries into a market already bleeding from other sellers. But here is the nightmare scenario. If the UAE unloads even a fraction of that, Treasury prices crater, yields explode, and Washington’s borrowing costs skyrocket overnight. The UAE would effectively detonate the very financial system it depends on. So instead, the UAE made a smarter, more desperate play. It went to Washington, and they essentially said, we did not start this war, but if you let us drown, we will have no choice but to sell your bonds, and you know exactly what that does to your market. Give us a currency swap line. Lend us dollars directly. Let us pledge our own currency as collateral and pay you back later. It is not a bailout of the UAE. It is a bailout of the Treasury market itself.

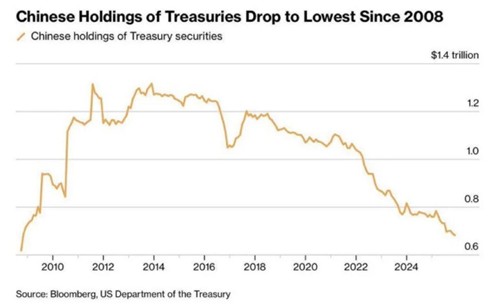

And the UAE is just the opening act. Kuwait exported almost zero barrels of crude in April 2026. For the first time in three decades, its oil taps ran dry. Kuwait Petroleum Corporation declared force majeure in March and extended it through April, telling clients flatly that even if the strait reopens, contracts may not be honored. Kuwait runs ninety percent of its government on oil money. Kuwait also holds $65 billion in U.S. Treasuries. Do the math. They will either sell into a falling market and trigger the spiral described, or they will follow the UAE to Washington’s doorstep with the same quiet threat. The roster of nations facing this choice will only grow as long as Hormuz stays closed. Washington is now playing a dangerous game of financial whack-a-mole, lending dollars to prevent the bond market from eating itself alive. The question is no longer whether more countries will need emergency liquidity. They will. The only question is whether Washington can keep writing checks fast enough to stop the Treasury market from unraveling. And what about the three largest holders? Japan, the United Kingdom, and China sit atop the foreign holdings with roughly $1.2 trillion, $700 billion, and $760 billion respectively as of early 2026. China is the wildcard, its holdings have fluctuated between $750 billion and $800 billion for years, a slow grind rather than a dramatic exit, reflecting Beijing’s careful calibration between reducing dollar dependence and avoiding a self-inflicted wound on its remaining portfolio. The Treasury market’s real devastating test will come not from Abu Dhabi or Riyadh, the real test will come from Tokyo, London, and Beijing . China just sold $40 billion last month.

The only remaining canary in the financial coal mine is the bond market. Equities can dominate the headlines and dance cheek-to-cheek with the Hormuz narrative, but US Treasuries continue to act as the central nervous system of the entire edifice. They are the collateral for every trade opened or closed every day, everywhere in the world. The bond market is what keeps the equity market at least minimally “real.” It is what serves as a reminder that this hyperinflated bubble is tied to the existence of real people. That is where real risk lives. In short, the stock market is driven by tech – tech depends on rates- rates stand on Treasury demand and Treasury demand is in a constant state of stress. Under the surface, a liquidity crisis is already brewing; one that is impossible to avert. The Bank of England’s recent short-term —a weekly auction where banks borrow cash from the central bank against collateral, and whose size spikes when banks cannot easily borrow from each other—was so large that, adjusted for the relative size of the UK and US financial systems, it would equate to a $300 billion drawdown at the Fed’s standing repo facility (that is, banks actively drawing that much cash from the emergency lending window, not merely having it available). That is double the peak drawdown of the March 2020 crisis, when global markets were freezing in real time. This is not just a footnote. This is the canary coughing blood. Remember the August/September Wall Street Repo Crisis. That eventually led to David Rockefeller Jnr puling the plug on the global economy in order to save the financial system. And the private credit market, in total silence, is bleeding redemptions with over $14 billion in outflows in the first quarter alone—a 146% increase from the previous quarter. JP Morgan is actively looking to offload exposure to $4 billion in private equity linked loans. If that amount is trivial, why offload it so publicly? Because the system is already cracking.

The Korean Won as Patient Zero?

As anticipated, the KOSPI has doubled in 2026. More than half these purchases were done with borrowed money. Among investors aged sixty to seventy, margin debt has more than doubled in the last year. These are quiet citizens who believed in fixed deposits and real estate for decades. Now they are borrowing to buy semiconductor stocks. —South Koreans torching their own life insurance to buy chips- up 16.3% from last year. Foreign smart money is already selling. Retail is buying with borrowed money and cancelled life insurance policies. And the net equity portfolio as a percentage of South Korean GDP has reached a frankly insane 12%. For context: that is the share of the country’s entire economic output that has been pulled into the stock market by domestic investors (ordinary citizens). No advanced economy has ever touched this number without a crash following shortly after. The Korean won is trading at levels last seen at the peak of the subprime crisis and before the tech crash of 2000. And the Bank of Korea has now decided to leave interest rates untouched at 2.5%, prioritizing the overleveraged stock market over the collapsing currency. Raise rates to defend the won, and the KOSPI pops. Do nothing, and the won keeps sliding. They have chosen to do nothing—a choice that confirms the central bank would rather let the currency burn than light the fuse under the stock market. The next fragile domino is Europe, including the UK, where a second serious liquidity crisis could force a financial crash in Europe, and then radiating outwards. One wonders whether, when the financial apocalypse comes, there will be anything real left to rescue.

Foreign Treasury Selling Is Getting Serious

We already knew that the bond market is about to break on America’s fiscal and monetary policy. Now we know that foreign governments are dumping U.S. Treasuries, and China is leading the way. Foreign holdings of U.S. government debt fell sharply in March as central banks sold Treasuries to defend weakening currencies during the geopolitical and energy shock tied to the escalating Middle East conflict. China reduced its Treasury holdings by $45 billion, and Japan, the single largest foreign holder of U.S. debt, also cut exposure aggressively. Overall foreign holdings dropped from approximately $9.49 trillion to $9.25 trillion in a single month. That should deeply concern anyone paying attention to the structural fragility underneath the U.S. financial system. Meanwhile, Japan is also undergoing a nasty financial squeeze. Its currency has weakened over the past year by some 70 %. To bring its value up, Japan is selling US bonds, and using the cash to prop up its currency. It has also raised interest rates to protect the yen. Good luck with both, as it has little chance of succeeding. But the damage it is doing to the “confidence “of the dollar by dumping US Treasuries is beyond measure. That system only works as long as there is confidence in the dollar and confidence that U.S. government debt remains the safest and most liquid place on earth to park capital. When major foreign holders begin reducing exposure during a period of rising inflation, exploding deficits, and growing fiscal instability, it creates a potentially dangerous chain reaction. And the timing for the world to be dumping treasuries right now could not be worse. Meanwhile, deficits continue spiraling, interest expense on the national debt keeps exploding higher, and the Treasury must issue enormous amounts of new debt simply to keep funding government spending. Now add weakening foreign demand on top of all of that. That combination is nasty. If foreign governments buy fewer Treasuries while supply continues surging, yields move higher. Higher yields tighten financial conditions across the entire economy. Interest rates stay elevated. Corporate refinancing becomes more expensive. Regional banks sitting on massive unrealized bond losses face renewed pressure. Commercial real estate weakens further. Consumers get squeezed harder. And because Treasuries serve as the foundational collateral layer of the global financial system, instability there spreads everywhere else. This is why the liquidation story matters far beyond geopolitics. the United States is issuing debt at an unsustainable pace into an environment where inflation is no longer fully under control. If that’s the case, that is not just a portfolio adjustment. That is a confidence signal. The uncomfortable reality is that the United States has become dangerously dependent on perpetual debt expansion at the exact moment global appetite for absorbing that debt is becoming less certain. As inflation reaccelerates while Treasury demand weakens simultaneously, the Fed faces two terrible options: raise rates further to defend credibility and contain inflation, risking deeper stress across banks, housing, private credit, equities, and the broader economy , or step back in with liquidity programs and money printing to stabilize markets and absorb debt issuance, effectively reigniting the same inflation problem they spent years trying to contain. That is the corner policymakers have backed themselves into after years of artificially suppressed rates, endless stimulus, and the assumption that global demand for U.S. assets would remain infinite regardless of fiscal discipline. It won’t. And once confidence in the system itself begins eroding, things can unravel far faster than policymakers would like. And now, beneath all the geopolitical noise, a much more serious, harder to ignore crisis is unfolding.

The 10-year Treasury yield is arguably the single most important price in global finance because virtually every major asset class is built on top of it. When yields rise too quickly, everything starts repricing at once. That is why this matters so much more than the daily moves in the stock market. Washington understands this, even if it refuses to say it publicly. The United States can survive political embarrassment overseas, but it simply cannot survive a disorderly Treasury market. That is why the bond market is eventually going to force a few things. First, a de-escalation of the Iran conflict. The priority now is no longer “victory” or even geopolitical strategy. The priority is restoring stability before bond yields spiral completely out of control. A prolonged war that keeps oil prices elevated while deficits explode higher is simply incompatible with a heavily indebted financial system already struggling under the burden of high interest rates. The problem is that America entered this conflict from an extraordinarily weak fiscal position to begin with. This is not World War II, when the country had a young population, industrial dominance, low debt levels, and decades of economic expansion ahead of it. Now add war spending, weakening foreign demand for Treasuries, rising commodity prices, and higher refinancing costs, and the entire situation starts looking dangerously unstable.

This is where the inflation problem becomes unavoidable. War has always been inflationary, but not just because of oil shocks or supply chain disruptions. The deeper issue is debt creation itself. The process is actually very simple: war creates debt, debt pressures the financial system, and eventually the system responds through some combination of money creation, currency debasement, and financial repression. That is exactly what the bond market is beginning to anticipate right now. In other words, the system may briefly attempt to defend the dollar before ultimately surrendering to debt realities. That creates the possibility of a brutal stagflation environment where growth slows, markets weaken, borrowing costs rise, and inflation remains stubbornly elevated at the same time. And that…is a nightmare scenario for risk assets. For years, markets became addicted to near-zero rates and endless liquidity. Entire sectors of the economy were built on the assumption that capital would remain permanently cheap. But when Treasury yields rise meaningfully, everything changes. Leveraged speculation becomes harder to sustain. Corporate refinancing becomes more expensive. Housing affordability deteriorates further. Commercial real estate faces additional stress. Equity valuations compress. The “everything bubble” suddenly starts losing oxygen and all the strategies, deals and plans will implode. And once again, the people who get hurt the most will not be the financial elite, it will be ordinary people. The Iran war may end sooner than many expect, not because global leaders suddenly become responsible, but because the bond market is forcing them into a corner. Financial instability is becoming the greater threat. Policymakers now face an impossible balancing act between inflation, debt servicing costs, economic slowdown, and geopolitical conflict. Something will have to give. Historically, when governments reach this stage, they choose to protect the debt market and sacrifice the currency. There is little reason to believe this time will be any different.

PPI came in at 6% (vs. 4.8% expected): The Producer Price Index measures inflation at the wholesale level, which means what businesses pay for materials, energy, and supplies before they become consumer goods. A 6% reading is “hot.” It usually signals that consumer inflation (CPI) is coming next, and that the Federal Reserve could be forced to raise interest rates to cool things down. Rate hikes are bad for stocks, especially tech stocks valued on future (expected) growth. This number alone should have sent Wall Street into a tailspin, but it didn’t. The U.S. Treasury sold $25 billion in 30-year bonds at a coupon above 5%—the first time since August 2007. What does that mean? A “coupon” is the interest rate the U.S. government pays to borrow money for 30 years. Paying 5%+ is expensive. The last time it happened was August 2007, right before the global financial crisis exploded. Higher bond yields compete with stocks: why risk your money in Nvidia when you can get 5% risk-free from Uncle Sam? More crucially: higher bond yields mean lower bond value. This is the inverse relationship that confuses many people. When yields go up, the price of existing bonds goes down. Think of it this way: you bought a 30-year Treasury last year yielding 3%. Now the government issues new bonds yielding 5%. Why would anyone buy your old 3% bond? They wouldn’t, unless you sell it at a discount, which translates as capital loss.

Now here’s where it gets dangerous. Banks, pension funds, insurance companies, and even the Federal Reserve itself hold trillions of dollars in U.S. Treasuries; not as investments to trade, but as collateral. They pledge these bonds to borrow money overnight, to meet capital requirements, and to back derivatives positions. When the value of that collateral drops, two things happen. First, anyone holding those bonds is suddenly sitting on unrealized losses. That’s exactly what triggered Silicon Valley Bank’s collapse in 2023: they held long-term Treasuries, yields spiked, bond values cratered, and depositors ran. Second, and more systemically: when collateral loses value, you can’t borrow as much against it. Across the entire financial system, that means less liquidity, forced asset sales to raise cash, and potentially a cascade of margin calls. In a worst-case scenario, institutions lose the ability to function. So, as well as being expensive for the Treasury, that 5% coupon was a silent markdown on every bond already sitting on every bank’s balance sheet. And that markdown is still spreading. So, here’s the bottom line. All the traditional indicators—from spiking bond yields to persistent wholesale inflation, collapsing market breadth, and record-low investor sentiment outside a handful of AI darlings—are screaming that a major dislocation is overdue. The only reason we haven’t seen a crash yet is a series of desperate, last-ditch financial games. But these are, at best, painkillers—certainly not the cure.

In emergency capitalism, the crisis never really ends; it just changes costume. Here are four costumes waiting in the wings.

1. A Treasury auction failure. If investors refuse to buy U.S. debt at any yield below, say, 5.5%, the government faces a liquidity crisis. No buyers mean no funding, which would lead to a forced Fed intervention.

2. A Japanese bond blow-up. Japan’s yields are also spiraling. If the Bank of Japan loses control of its yield curve, it would trigger a massive unwinding of the yen “carry trade” (where investors borrow cheap yen to buy U.S. assets). That reverse flow would dump billions in U.S. stocks overnight.

3. A “slow motion” margin call on tech – the leveraged bets piled beneath them (via derivatives, options, and synthetic ETFs) could unwind in a cascade, turning a routine correction into a fire sale.

4. A war-driven energy shock that forces a recession first, and then a desperate Fed pivot. Here’s the story everyone seems to be misreading. If the Iran conflict widens, oil could spike to $200-250+/bbl. if the shock is severe enough to crater demand (factories idle, unemployment jumps, consumers disappear), “money velocity”—the speed at which cash changes hands—collapses. People hoard, businesses stop investing, and inflation suddenly turns into disinflation, or even deflation.

A few bank bankruptcies are manageable, but an interest rate shock to the massive derivatives market could take down the whole economy. Will rapidly rising interest rates rip through the U.S. financial system like a giant lawnmower blade? Yes, the U.S. economy survived much higher interest rates in the past, but at that time there were not hundreds of trillions of dollars’ worth of interest rate derivatives hanging over our financial system like a Sword of Damocles.

Rising interest rates could burst the derivatives bubble and cause massive bankruptcies around the globe if they go down, our entire economy will go down with them. … Our entire economic system is based on credit, and just like we saw back in 2008, if the big banks start failing, credit freezes up and suddenly nobody can get any money for anything.

Controlled Disintegration

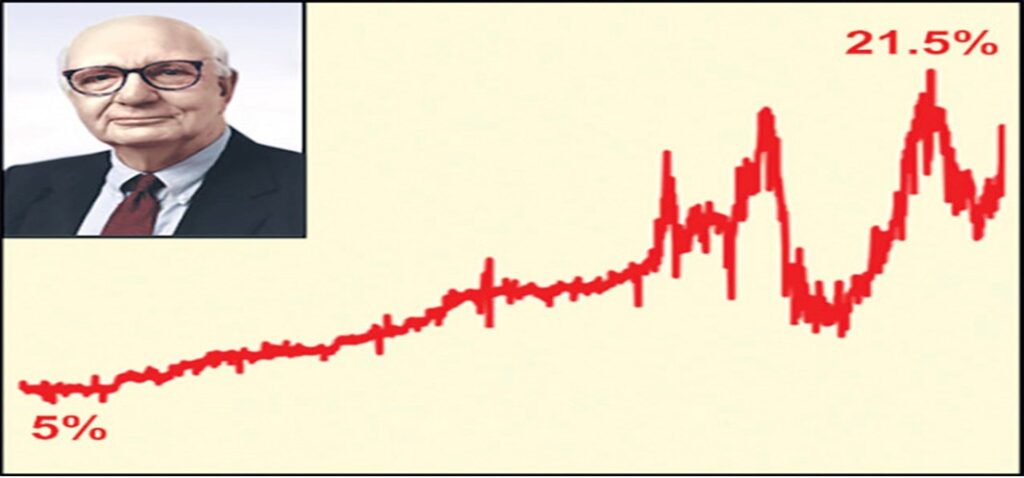

Mankind’s existence is based on the fact that mankind is the only species of which we know which has the willful power to increase the energy-flux density of life as a whole on our planet Earth—and beyond. There are many indications that point in this direction. the increase in energy-flux density throughout the planet is the precondition for the survival of any species. Any species that does not rise to a higher level—to progress to greater energy-flux density—perishes. The Rockefeller family has demanded that the human population of the planet be reduced from current levels. This is the official policy of the US Government. It’s a policy of mass murder. And the fact of the matter is that mankind’s ability to exist as a species is based on the fact that mankind is able to increase the energy-flux density which we are able to apply to the existence of human beings on this planet. Those who have a contrary view—I’ll call them the oligarchical system. The oligarchical system is a bunch of fruitcakes, to use the term politely, who believe that mankind is divided into two groups of people: a small but “honorable” group of people who believe that there are too many of the lower folk, and we have to reduce and keep down the number of lower-class folks in order that the degenerates who call themselves oligarchs will be able to enjoy themselves more freely. So, the issue here is that the destiny of humanity depends upon increasing the energy-flux density per capita. It means increasing the size of the human population. Without those measures, there is no future. And the oligarchs will have to become extinct if they continue their policies. Those nations that invest in the physical economy- infrastructure- will, over time, become more prosperous than those nations that neglect physical economy. We emphasize physical economy because Man’s productive activity is actually a living process. If one significant area of that process is destroyed, the entirety will tend to collapse in a nonlinear fashion. This is what some observers refer to, simplistically, as a “supply chain” effect. For any country to benefit from an increase of physical economy, interest rates have to be kept very low. A high interest regime does not allow for the build-up of infrastructure. The price of oil in 1972 was $2 a barrel. By 1974 it increased to $12. By 1979, the CIA/M16 toppled the Shah of Iran and installed Khomeini into power. The oil markets went crazy, and by 1980, the oil price had shot up to $30! These increases drove up inflation in the world. Paul Volcker was an employee at David Rockefeller’s Chase Manhattan Bank. In 1978 David promoted him to the chair of the Fed, with one mandate- bring down inflation. In a speech on November 9, 1978, Paul Volcker, who was then the head of the Federal Reserve, Volcker said the following: “A controlled disintegration in the world economy is a legitimate object for the 1980s.”

The graph below indicates what Volcker did when he was given the reins at the Federal Reserve. By December 1980, he had raised the prime lending rate in the United States to 21.5%. As is documented, the effect of 21.5% interest rates was a collapse, on a per-capita basis, of U.S. machine-tool production by 45%, bulldozers by 53%, automobiles by 44%, steel by 49%, and so on. This was intentional, and it was controlled disintegration. The aim was to end the industrial manufacturing base of America, first, followed by Britain, and from there, radiating outwards to the rest of the world.

Now, let me just give you an idea of what this policy actually is, and where it began. The effect of this on less developed countries, the so-called Third World, was a disaster, which resulted in what we have called “Bankers’ Arithmetic.” Interest rates were raised so high that the more Third World countries paid, the more they owed. Take the case of Brazil.

Brazil: Bankers’ Arithmetic

In 1980 Brazil owed $72 billion in foreign debt. Over the course of the next 18 years, through 1998, they paid $146 billion in interest payments alone. They paid more than double what they owed! And after that process was over, they hadn’t paid off the debt; rather, the debt had risen to $231 billion. In other words, $72 billion minus $146 billion is equal to $231 billion. That only happens under bankers’ arithmetic. Now, where did this policy really come from? It didn’t come from Volcker. It came from a study that was prepared by something called the 1980s Project, launched by the Council on Foreign Relations of New York, which in 1977 published a 33-book series, one of which was called Alternatives to Monetary Disorder. This, in turn came from a future policy book written by David’s eldest brother in 1971/2, called the “Second American Revolution “, published in 1973. This was the blueprint of the Rockefeller family for the world for the next 3 decades. And, from this book emerged such totalitarian ideas as “controlled disintegration”, the “China policy”, and the move to establish the “Petro-dollar”, amongst other policies enacted by the family over the ensuing decades. This 1980s Project study,became the policy of the Carter and Reagan administrations.

Controlled Disintegration and Malthusianism

You may recall that Thomas Malthus wrote such comments as the following from 1791, where he encourages the reduction of the population, and if necessary, as he said, to “court the return of the plague” as a necessary means for reducing the population—intentionally. This didn’t stop with Malthus. Bertrand Russell said the exact same thing in 1951, Betrand Russell, too, called for a Black Death to spread throughout the world:” War has hitherto been disappointing in this respect [population control], but perhaps bacteriological war may prove effective. If a Black Death could spread throughout the world once in every generation, survivors could procreate freely without making the world too full.” And more recently, Prince Philip, who you may recall was the father of King Charles III of the United Kingdom today, Prince Philip in 1988 said: “The more people there are, the more resources they’ll consume, the more pollution they’ll create, the more fighting they will do. We have no option. If it isn’t controlled voluntarily, it will be controlled involuntarily by an increase in disease, starvation and war…. In the event that I am reincarnated, I would like to return as a deadly virus, in order to contribute something to solve overpopulation.” Population control is, unfortunately, an ongoing policy today. It was explicitly stated in Henry Kissinger’s National Security Study Memorandum 200, completed on December 10, 1974 but not made public until much later, which stated: “We have to provide assistance for population moderation in various countries”—in other words, reduce the population. The countries that NSSM-200 names are India, Bangladesh, Pakistan, Nigeria, Mexico, Indonesia, Brazil, the Philippines, Thailand, Egypt, Turkey, Ethiopia, and Colombia. And I’m sure that since that was written, Iran has been added to that list, de facto. And what the document says, in their own words, in Kissinger’s words: “The real problems of mineral supplies [which the West needs—ed.] lie not in basic physical sufficiency, but in the political-economic issues of access – In the extreme cases where population pressures lead to endemic famine, food riots, and breakdown of social order, those conditions are scarcely conducive to systematic exploration for mineral deposits or the long-term investments required for their exploitation.” I’ll translate that for you into plain English: “They have the minerals. If we let their population grow, they’re going to want to use the minerals. We’re not going to let that happen. We want those minerals. Therefore, we will reduce their population.” In short, the aim to reduce the global human population through famine, biowarfare, poor economic conditions, etc. is a Rockefeller family policy. A major structural change is occurring. After decades of globalization and optimization, nations are increasingly adopting protectionist policies and trade barriers. This fragmentation is pushing up costs, reducing the efficiency of global supply chains, and curbing shared global growth. What is coming now in the coming months, barring a dramatic policy reversal, is the worst economic depression in history to date. Thank you, globalization.

Globalization

The political pressures behind globalization and the creation of the World Trade Organization out of the Bretton Woods GATT trade rules with the 1994 Marrakesh Agreement, ensured that the advanced industrial manufacturing of the West, most especially the USA, could flee offshore, “outsource” to create production in extreme low wage countries. No country offered more benefit in the late 1990s than China. China joined WHO in 2001 and from then on, the capital flows into China manufacture from the West have been staggering. So too has been the buildup of China dollar debt. Now that global world financial structure based on record debt is all beginning to come apart. The August 1971 Nixon decision to decouple the US dollar, the world reserve currency, from gold, opened the floodgates to global money flows. Ever more permissive laws favoring uncontrolled financial speculation in the US and abroad were imposed at every turn, from Clinton’s repeal of Glass-Steagall at the behest of Wall Street in November 1999. That allowed creation of mega-banks so large that the government declared them “too big to fail.” That was a hoax, but the population believed it and bailed them out with hundreds of billions in taxpayer money. Since the crisis of 2008 the Fed and other major global central banks have created unprecedented credit, so-called “helicopter money,” to bailout the major financial institutions. The health of the real economy was not a goal. In the case of the Fed, Bank of Japan, ECB and Bank of England, a combined $30 trillion was injected into the banking system via “quantitative easing” purchase of bonds, as well as dodgy assets like mortgage-backed securities.

The story continues in Part 2.