– – we are continuing from the previous article.

The Starting Point

The fact that CBDCs are intended as financial shackles to control you within what amounts to an open-air prison is also noted by South Dakota Gov. Kristi Noem in a Fox News interview. She highlights a proposed Uniform Commercial Code (UCC) update that seeks to redefine “currency” to exclude decentralized crypto currencies, effectively putting the government on the path to a CBDC monopoly. Noem vetoed the bill and is urging other states to reject it as well.

The UCC Code is a set of laws that govern commercial transactions in the U.S. While not a federal law, it’s a set of laws that states agree to adopt in a uniform fashion to facilitate interstate business. So, it appears they intend to begin the financial takeover by rolling out the CBDC on the state level first, and legislators who believe in freedom must denounce all such plans. This is what most observes must look for, as it will signal the start.

All Banks, Including the Fed, Are Likely Insolvent

While the economy was good, banks earned hefty profits from these toxic assets, but as soon as the economy downshifted, these toxic securities plunged in value and wiped them out. This time, however, the toxic asset is U.S. government bonds that are sinking banks, and these bonds are supposed to be the safest investment there is.

According to FDIC estimates, the unrealized losses of U.S. banks is approximately $650 billion (as at end March) and rising. Meanwhile, the FDIC’s deposit insurance fund (DIF) has a balance of just $128 billion. See the problem? What’s worse, the DIF money doesn’t just sit there. It too is invested — in U.S. government bonds!

And it’s only going to get worse if the Federal Reserve continues to increase interest rates. The problem is, interest rates need to be raised to curtail runaway inflation, but if they go up, more banks will sink due to their holdings in government bonds. There’s just no way out. The people of NATO-land, and in particular the U.S., must stop acting like vassals to a political elite that hold unchallenged power, and defend their right to contribute something of enduring benefit to the future of mankind as a whole.

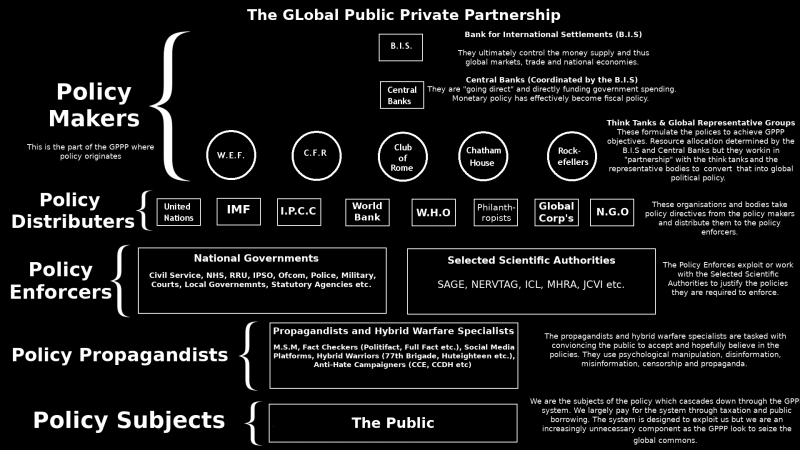

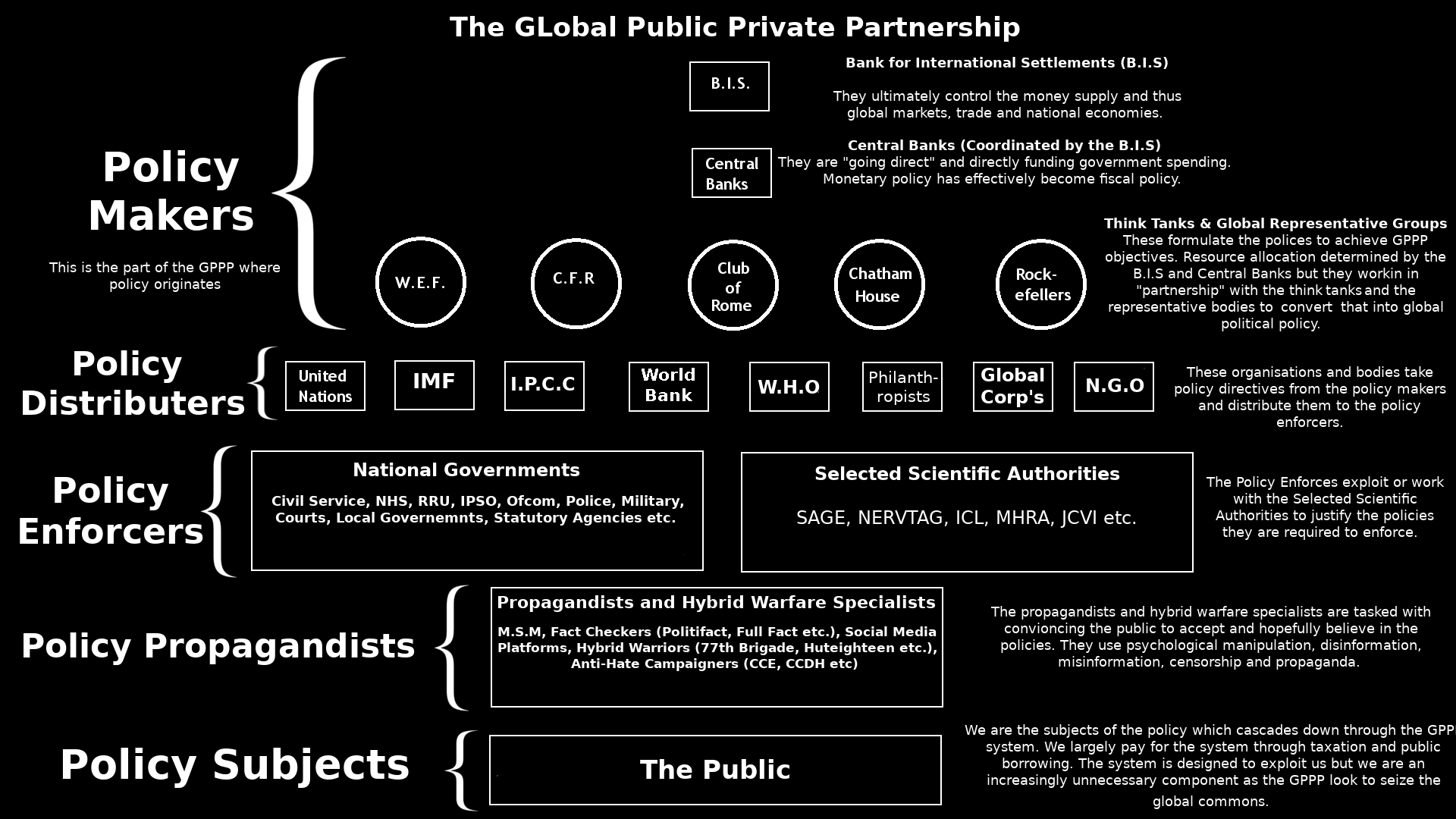

The Fed has become the Central of the World!

The US Federal Reserve System was started in 1913. It was a Rothschild project from day 1. But, for this new system to work effectively within the US, it needed America’s richest and most powerful family on board – they had to take in the Rockefeller family on as a partner/shareholder. This project was a joint operation of the 2 families. The ownership was split – one third for the Rockefellers and two thirds for the Rothschilds.

In October 2000, a key Rothschild bank, JP Morgan went bust trough derivative losses. Rockefeller’s Chase Manhattan bought it. With this purchase came JP Morgan’s holdings in the US Fed, which was some 17%. With this purchase, the Rockefeller family now had CONTROL OF THE US FED! And, since the Fed is the most powerful central bank in the world, the Rockefeller family would use this power in devastating ways- in order to enhance and solidify their control and power over rivals. The family motto “COMPETITION IS A SIN”- is part of DNA of the family members. David Rockefeller Jnr is going to take this to the next level. And this is how it is going to be done.

Banks are made up of 3 separate and distinct components. It is the shareholders, bondholders and depositors. Of the 3 components, the bondholder is key. Silicon Valley is an example of how it is going to be implemented: – Shareholders are cancelled. Depositors are made whole. Of the bondholders, the majority are fronts for the Rockefeller Empire. We will discuss this aspect of “bonds” when we are doing the article, titled DOPE INC- the report of the international narcotics trade- which is a fully-controlled by the 2 families.

The bondholders will call the shots. While the depositors will flee the 4,000 regional banks to the 5 mega banks- of which 4 are in the Rockefeller orbit. Bank of America is a Rothschild bank. While JPMorgan Chase, Citicorp, Goldman Sachs, Wells Fargo are in the Rockefeller orbit. It will be at this point that the “plug will be pulled”. Banks close. The financial systems freezes over, then shuts down.

Now, what I don’t know at his time, will be the period between bank shutdown, and the “re-opening” of banks under the new system of digital currency. There will be no more retail institutions. Banks, as we know it, will cease to exist. The Rockefeller family has eliminated the competition. The process in Europe is slightly different. It will be the US FED, and you- government, business and individuals. This will then make David Rockefeller Jnr the unofficial and uncrowned “KING OF AMERICA”.

Remember, “COMPETITION IS A SIN”.

Federal Reserve vice chair Lael Brainard had said that if CBDCs were widely adopted, it would disrupt the entire banking system because people would make direct central bank deposits bypassing retail institutions. Although Fed researchers claim CBDCs offer a “helpful competition to the banks,” CATO concludes that the most probable outcome will be people leaving traditional banks as “it is difficult (if not impossible) to compete with the government.” In such a scenario, CBDCs will have a monopolistic hold over the market.

FedNow and CBDC

On March 15, the Federal Reserve announced the FedNow Service, which will start operating in July. FedNow offers a nationwide “instant payment solution” for participating financial institutions and their industry partners. Those using the service can “send and receive instant payments at any time of day” with full access to funds immediately.

Fed governor Michelle Bowman said last year that FedNow could weaken CBDC-resistance via offering some of the same basic services of a digital dollar—a first step toward full CBDC adoption. FedNow appears to be a prototype CBDC which can quickly transform to a surveillance system.

The Bankers’ Nightmare

Following the global financial crash in 2008, which was caused by the commercial banks profligate speculation on worthless financial derivatives, the central banks “bailed-out” the bankrupt commercial banks by buying their worthless assets (securities) with base money. The new base money, also created from nothing, remained accessible only to the commercial banks. The new base money didn’t directly create new broad money. This all changed, thanks to a plan presented to central banks by Blackrock. In late 2019, the G7 central bankers endorsed BlackRock’s suggested “going-direct” monetary strategy.

BlackRock said that the monetary conditions that prevailed as a result of the bank bail-outs had left the International Monetary and Financial System (IMFS) “tapped out.” Therefore, BlackRock suggested that a new approach would be needed in the next downturn if “unusual circumstances” arose. These circumstances would warrant “unconventional monetary policy and unprecedented policy coordination.” BlackRock opined: Going direct means the central bank finding ways to get central bank money directly in the hands of public and private sector spenders.

Coincidentally, just a couple of months later, the precise “unusual circumstances,” specified by BlackRock, came about as an alleged consequence of the interest rate hikes. The “going direct” plan was implemented.

Instead of using “base money” to buy worthless assets solely from commercial banks, the central banks used the base money to create “broad money” deposits in commercial banks. The commercial banks acted as passive intermediaries, effectively enabling the central banks to buy assets from nonbanks. These nonbank private corporations and financial institutions would have otherwise been unable sell their bonds and other securities directly to the central banks because they can’t trade using central bank base money.

The “Essential” CBDC Public-Private Partnerships -The IMF leads The Way

CBDC will only be “issued” by the central banks. All CBDC is “base money.” It will end the traditional split circuit monetary system, a.CBDC potentially cuts commercial banks out of the “creating money from nothing” scam.For CBDC to be successful, it would need to be widely adopted: Today, April 10th, the IMF(a Rothschild entity) has just launched a new global currency , but 99.99 % of the global population has no idea what just happened.

The “Universal Monetary Unit”, also known as “Unicoin”, is an “international central bank digital currency” that has been designed to work in conjunction with all existing national currencies.

The IMF did not create this new currency, but it was unveiled at a major IMF gathering earlier this week…Universal Monetary Unit (UMU), symbolized as ANSI Character, Ü, is legally a money commodity, can transact in any legal tender settlement currency, and functions like a CBDC to enforce banking regulations and to protect the financial integrity of the international banking system.

As the press release quoted above indicates, this new “Universal Monetary Unit” was created by the Digital Currency Monetary Authority.

So who in the world is the Digital Currency Monetary Authority? The DCMA is a world leader in the advocacy of digital currency and monetary policy innovations for governments and central banks. Membership within the DCMA consists of sovereign states, central banks, commercial and retail banks, and other financial institutions. Basically, just another outfit created by the 2 families to “co-ordinate” the introduction of this into the global financial system. Basically, it sounds like the 2 families and vassal national governments are conspiring to push this new currency down our throats. We are being told that the “Universal Monetary Unit” is “‘Crypto 2.0” and those that created it are hoping that it will be widely adopted by “all constituencies in a global economy”… Of course the Digital Currency Monetary Authority is not the only one that has been working on a new digital currency. The UK has also been working on one. The same is true for the European Union. And would it surprise anyone that the Biden administration is touting the potential benefits of a “digital form of the U.S. dollar”? The following comes from the official White House website…

A United States central bank digital currency (CBDC) would be a digital form of the U.S. dollar. it is not a coincidence that governments all over the western world are simultaneously developing CBDCs.

The International Monetary Fund (IMF) is putting together a Central Bank Digital Currency (CBDC) handbook to assist central banks and governments throughout the world in their CBDC rollouts.

But it is imperative to understand that once everyone is using them, your financial privacy will be almost totally gone. Can you imagine a world in which you are restricted from buying meat for a while because you have already used your “carbon credits” for the month? Of course in order for such a system to have real teeth, cash and other forms of payment will need to be phased out and that is precisely what is happening right now in Europe. To restrict transactions in cash and crypto assets, MEPs want to cap payments that can be accepted by persons providing goods or services. They set limits up to €7000 for cash payments and €1000 for crypto-asset transfers, where the customer cannot be identified. Ultimately, they will just keep lowering the limits until the use of cash is almost completely eliminated. Everyone will be slowly but surely forced on to the new digital system and it will be a system that they control with an iron fist.

Inflation, economic instability and a lack of savings have an increasing number of Americans feeling financially stressed. 70 percent of all Americans are “financially stressed” at this point. Most Americans simply do not care that these new digital currencies could open a door for great tyranny. They just want to be able to pay the bills and take care of their families, and if our politicians tell them that this new system is good for the economy they will be all for it.

Concentrating even more power in the hands of the international elite is always a bad idea, and hopefully we can start to get more people to understand this.

The circus surrounding the arrest of former President Donald Trump may have been a perfectly well-timed distraction. Not only are our banks still in a state of collapse despite a brief government-funded reprieve. Not only is the advent CBDCs looming over us. But, the world is rapidly dumping the dollar, and that’s a next-level economic disaster.

There is a movement away from the dollar in international trade. We will explain how this is also adding to the impetus to usher in this CBDC. A lengthy list of countries are moving away from using the US dollar, which has long been the reserve currency of the world. The following countries are in the process of reducing their dependency on the dollar- Russia, China, Iran, Brazil, Argentina, Saudi Arabia, and Malaysia. Most are going ahead trading with their own currency.

Any non-American entity or individual that uses US dollars to trade, they pay a “fee” of 3%. This is besides bank fees and interest costs. By-passing the dollar in trade eliminates this hidden cost.

So, for this reason, plus the fact that most countries are tied into the dollar system, the Global South countries, have woken up to the fact that Washington can do the following to their countries , if they refuse to obey orders :- Washington imposes sanctions, a SWIFT cut-off, freezing of assets, etc. This would be to the detriment of that country and government. With this realization, most of the Global South or Zone B nations are de-dollarising. This is accelerating, forcing the Fed to push up interest rates in a vain attempt to plug the dam before it bursts. If that were to happen, there would be a complete implosion of the global economic system, but certainly the American economic system. And if that were to happen, you’d be looking at sky-high inflation just raging, Weimar Republic kind of inflation. If you think inflation is bad right now, just wait. But more importantly, the US would lose its economic dominance and its superpower status.

Like I stated earlier, the Rockefeller Empire is ready for the withdrawal of foreign investments within the US capital markets. What would happen if foreign investors’ withdrawal from US capital markets is not allowed? Once CBDC becomes a fact, foreign investors will then be offered these electronic blips. Would they accept? Definitely not! Things were stable the dollar was backed by gold. After 1975, it was backed by oil. Now, once again, we are at a turning point. The dollar will be backed by electronic blips – a series of 0s and 1s. As Putin recently stated. One can’t buy energy or food with paper. It gets worse with 0s and 1s.

All of this is why it’s so important to prepare and become as independent as possible. The things we’ve taken for granted our entire lives may soon vanish, and what’s coming to replace them are not in your best interest unless you’re part of the globalist cabal that will exempt themselves from the slave system.

The End-Game

So, putting all these factors together, we find that the race in trying to save the financial system and their banks is on. Will time be on their side?

Due to the death of globalization, we find that the world is splitting up into two distinct economic/security and political blocs; The Collective West or Zone A, and the Global South, or Zone B or the Eurasian Alliance. The introduction of the CBDC will work in the West, and not the East. The 2 families have a tight grip on the West, and can count on governments to do their bidding. Only one question remained. Would ice-nine work? There was no doubt about government’s capacity to impose ice-nine. Still, would citizens give in as they had previously, or would there be a descent to disorder? If money riots broke out, authorities in the western world were prepared for that too.

The US has been under a state of emergency since September 14, 2001. The state of emergency grants the American president extraordinary powers, including martial law. Similar laws have been passed in Canada, Europe, Australia, New Zealand, Japan, and India. This is not the stuff of conspiracy theorists.

The use of these emergency powers and martial law is a more coercive version of the ice-nine plans to freeze accounts in place. Ice-nine is intended to buy time and restore calm while elites work on plans to allocate losses and reliquify the system. If events spin out of control faster than elites expect, more radical measures may be needed. Such measures may involve property confiscation. If resistance is encountered, martial law backed up by militarized police will carry out the orders of the head of state.

Emergency powers will not be used in a containable financial crisis of the kind we saw in 1998 and 2008. Yet that is not the kind of crisis we are facing. The next financial crisis will be exponentially larger, and impossible to contain without extraordinary measures.

As the next crisis begins, and then worsens, measures described here will be rolled out, one by one. First comes asset freezes and exchange closures. Then confiscation backed up by armed force. The question arises – will everyday citizens stand for it?

During the 1997-98 global financial crisis, riots in Indonesia and Korea left many dead. There was blood in the streets. Since the 2008 financial crisis, there have been violent protests in Greece, Spain and Cyprus that have resulted in many deaths. In the next crisis, as confiscatory solutions are employed, the popular response is likely to involve resistance.

Elites are prepared for this also. Washington has a classified plan for continued operations of the government during attack, financial collapse, or natural disasters. This combination of emergency facilities and powers means that the US government is ready for a catastrophe. The American people are not. And exactly the same sort of emergency facilities and emergency powers have been put into place by all the western governments – and done very quietly.

A global financial crisis, worse than any before is imminent. A liquidity injection of the kind seen in 1998 and 2008 will not suffice because central bank balance sheets are stretched. There will be little time to respond. Ice- nine account freezes will be used to buy time, but investors will grow impatient with ice-nine. They will want their money back. The money riots will begin. It will be at this point in time that the 2 families will roll out the CBDC. This may help quell some of the anger. But, many others who had seen their entire life’s savings evaporate, their property confiscated, their businesses shut for good, they will become more violent. Governments would not go down without a fight. The response to money riots will be confiscation and brute force. Governing elites will be safe in their heavily guarded mountain, or island retreats, or heavily fortified gated communities. No doubt about it, a global financial lock down will be followed by blood in the streets. There is no force on earth that can stop the desperation of a hungry stomach. Are you ready for this? Are you making preparations for this?

A last point to consider is that if this gamble of theirs fails, then the only thing left is for David Rockefeller jnr to initiate global thermonuclear war. Our next article is called “France & the Rockefellers”.

{kind=link}

{kind=link}

new website: behindthenews.co.za

new website: https://behindthenews.co.za/