The Fed Tightens

As a result of the Fed’s relentless tightening blitz, both US capital markets (the S&P 500 is down -24%, and 10 year US treasuries are down -17% and bonds were down -10%) and the US economy have been left reeling. One should note –WHY IS THE FED RAISING INTEREST RATES? The day that Putin announced 2 measures, 1- that sales of Russian energy will be done in rubles and, 2- that the ruble will have gold backing. This was in the first week of March. This one announcement signaled the demise of the dollar. Since then, money began to flee from the US dollar. By early May, it was becoming clear to the world that America was a paper tiger. It was losing militarily in Ukraine against Russia; it was losing economically as it has moved away from producing goods (physical economy), and lastly, the dollar was the only thing holding up the American Empire. A currency backed by “confidence”, versus a currency backed by gold AND HARD RESOURCES. No contest.

To add to the loss of trust, the last straw for many was the theft of assets belonging to its rivals (Russia, Afghanistan, and Venezuela). This proves to many that putting your money in the dollar is suicidal, and none of them want to see their assets seized. Today, one is a friend of America. Tomorrow, that same friend is an enemy. Many international investors began to lose confidence in the US dollar. When a currency like the dollar loses the confidence of its buyers and holders, then the end is around the corner. Due to Russian commodities being priced in non-dollar currencies, means that less dollars are needed. It’s been 8 months since Putin’s announcement.

Now, what happens to all those “unwanted” dollars? They return home to Mama.

This wall of dollars returning to the American economy is now circulating within the economy, and driving up prices. More money chasing the same volume of goods. Naturally, prices will go up. To add insult to injury, there has been a DECREASE in the PRODUCTION of goods. So, more money is chasing even fewer goods. The result? Soaring inflation. Over the next year, we see that Turkey, India, China are buying increasing volumes of Russian goods using a mixture of the ruble and their own currencies.

This means even larger volumes of “unwanted” dollars coming home to roost. The FED, in trying to contain the dollar’s destruction, has been forced to raise interest rates in order to do 2 things. 1- to stop money fleeing the dollar and, 2 – to pull in monies from around the world in order to “shore up confidence” in the dollar. This has succeeded to date, as the FED rates are 4%, while the rate in the EU and Japan is at 0.25%. No contest. Other central banks also raised rates in a bid to hold onto their currency reserves. And the FED is not going to stop. They have no choice. If they do, then the next thing is, “prepare for the funeral”.

However, the damage in the US – whose economy is relatively isolated from the knock-on effects of the soaring global reserve currency – are nothing compared to the global devastation unleashed by the Fed in the form of the soaring dollar and exploding interest rates.

In a startling outcry breaching the unspoken protocol of “no dissent, never dissent”, Josep Borrell, the high representative of the 27-member EU bloc, lashed out all too publicly at the Fed when he said that central banks (across Europe where the recession will be far, far worse than in the US) are being forced to follow the Fed’s multiple rate rises to prevent their currencies from slumping against the dollar. This time however, there is no simple solution in taking advantage of gullible states, instead now that they’ve broken the seal of silence, the “leaders” of Europe admit to just how powerless they truly are when the custodian of the world’s reserve currency has to do what’s best only for itself – allies and friends be damned: “Everybody has to follow, because otherwise their currency will be [devalued], Everybody is running to increase interest rates, this will bring us to a world recession.” Yes, the artificial facade of calm agreement propping up the world’s most aggressive tightening cycle in history is starting to crack and quite violently at that.

The Euro was an even worse disaster: at least in the pre-euro days, European countries could devalue their way out of a fiscal crisis; with the common currency they all have to beg the ECB for bond-buying mercy. A portfolio manager at one of Germany’s largest insurance companies who summarized recent events: “It’s a global margin call. I hope we survive”.

Since then it’s gotten from bad to worse as weaker European banks suddenly have trouble finding short-term funding, in the process sending the cost of Credit Suisse borrowings are higher than it was in 2008, at nearly 4 percentage points above the cost of interbank funding, prompting even more questions about European bond market stability and speculation that the ECB will be the next to capitulate and bail out markets.

Credit Suisse ironically was just named (Sept 27) “derivatives house of the year” in the 2022 Asia Risks Awards. It has taken its third big derivatives bath in 2 years –Archegos liquidation; Greensill liquidation; now interest rate derivatives losses. Its CDS now cost nearly $400 per $1,000 in credit, but it’s been worse, and Deutsche Bank still is worse. Remember we’re in a case of a $500 trillion in derivatives, meaning at least $5-10 trillion is immediately at risk of loss, and there 100s of major counterparties in the financial system.

The British Bond Collapse – When Financial Systems Fail.

Financial systems are man-made. History has shown, time and again, that all financial bubbles eventually pop. And that is what is happening right now. The biggest bubble in known human history, the parasitical, financial system of the Western oligarchy, which has dominated the globe for centuries, is popping, and we are headed for a major financial collapse in the short-term. The financier “boys in the back room “are now openly discussing the likelihood of imminent systemic financial breakdown. Risks to the financial stability of the EU banking system may materialize simultaneously, thereby interacting with each other and amplifying each other’s impact. Only once did they mention the elephant in the room: the nearly $2 quadrillion in pure financial gambling debts upon gambling bets, which is now blowing out. They offered no solution.

The Rothschilds are very worried that the financial system cannot simultaneously bail out their financial system AND carry out its strategy of bringing down hyperinflation by raising interest rates, restricting money printing and crushing economic activity at the same time. The British treasury is looking at a budget hole of 50 billion pounds. In short, the British government, currently, is beyond broke. Adding to this is the energy subsidies that will come to some 50-7- billion pounds. Where is the money going to come from? So, rather than give up their oligarchic system, as has often also happened in history, today’s financial oligarchy – the interests grouped around the two families – are all-in on a high-risk gamble that their control can be saved through global war, “democratic dictatorship”, and mass starvation.

What is happening is so unbelievable, that the idea that all of that is going smoothly, that to continue with operations as they are, is ludicrous? What we see is the unraveling of almost everything, and at the same time, the formation of a completely new system.

London Trying to pull the fuse out of Swaps Time Bomb

THE BOE acknowledged that a systemic financial crisis was beginning; triggered by interest rate derivatives, when on Sept 28th the Bank announced a return to QE with more than $70 billion to buy long-term British government bonds from big banks. The testimony described these stages of the crisis:

- British government bonds (gilts) suddenly plunged in value (their interest rates spiked) after the Truss government made completely incompetent energy-bailout and tax-cut announcements;

- Large number of pension funds were “hours from collapse” late on Sept 27;

- Complete panic hit the $1.69 trillion so called “liability –driven investment(LDI) pension funds ;

- The BOE was informed by a number of LDI fund managers – – – that these funds would have to begin the process of winding up the following morning ;

- A “large quantity of gilts, held as collateral by banks that had lent to these LDI funds, was likely to be sold on the market, driving a potentially self-reinforcing spiral and threatening severe disruption of core funding markets and consequent widespread financial instability “; the BOE worked through the night on Tuesday 27th – – to achieve this potential crisis;

- The London Rothschilds (the City of London, BOE, and the ECB) are escalating the demand that the Rockefellers (the Federal Reserve) join the return of QE before it’s too late. The financial systemic blowout threat they are warning of, requires the control of derivatives, now particularly interest rate derivatives.

- Interest rate derivatives make up 82 % (as of end 2020) of all OTC derivatives globally, $495 trillion out of $600 trillion. But to trigger the 2007-2008 global financial crash, “just “

- $65 trillion in credit derivatives (CDS) exposure was sufficient. The central counterparty in 90% of current interest rate derivative exposure is a bank or non-bank financial institution. Because of the Fed, the margin calls for collateral which wiped out liquidity in the commodity trading-producing sector in March-April (war and sanctions), has now spread to the far, far larger sector of institutions and funds which use interest rate swaps, and their banks.

The BOE returned to QE in order to bail out more than $2 trillion in pension funds’ assets of “liability-driven investing” in the UK alone. LDO consists in making pension fund “assets” out of interest rate derivatives. These pension funds were earning around 1% (in the environment of low interest rates), and borrowed money from banks in order to gain a bigger return by investing in the stock market, etc. When markets are in decline, banks were requesting more collateral to cover their loan values. This situation became worse when the underlying collateral began to fall in value after the disastrous Truss announcement. So, the Fed, which led the central banks in creating runaway inflation from September 2019 onward in order to write off unpayable debt, to trigger a deep global recession, crush developing economies, and light a time bomb in at least $500 trillion at risk in interest rate derivatives.

The BOE has acted to bail out the derivative fake values of Brits’ pension funds, while the UK government wipes out their living standards and savings by war and financial war on Russia. LDI “asset building” has also been sweeping by big US firms’ pension strategies since 2015. And not just today’s latest collapse in UK bonds:, risk in Germany’s government debt market rose last week to levels higher than recorded in the 2008 world financial crash, as margin calls forced the liquidation of derivatives positions held by banks, insurers and pension funds.

- “Real” yields, namely the yield on inflation-indexed government bonds, went deeply into negative numbers in Germany and the UK, followed by the US market. That pulled the rug from under insurance companies and pension funds, which invest pension payments and insurance premiums to provide for future income.

- To compensate, European and UK institutions locked in long interest rates with derivative contracts, or interest-rate swaps that receive a long-term interest rate while paying a short-term interest rate. Swaps are a leveraged position that requires collateral worth a fraction of the notional amount of the contract.

- When the Fed jacked up interest rates in late 2021, the value of interest rate swaps that pay fixed and receive floating rates imploded. Pension funds and insurers were stuck with the equivalent of a ten-to-one margin position in long government bonds. The price of long government bonds fell by nearly 20% across the Group of Seven countries, and the value of derivatives contracts evaporated.

And that left UK institutions facing a tsunami of margin calls that they could meet only by liquidating assets. That in turn led to a run on the UK government bond market, followed closely by the rest of European bond markets. The Bank of England’s emergency bond-buying delayed a market crash, but the UK gilts market remains on a knife edge, with option hedging costs at an all-time high.

The UK bond market stabilized when the BOE capitulated and restarted QE. In the process, Jacob Rothschild fired Liz Truss, as he saw her as responsible for this debacle.

What about the US?

So far, American pension funds and insurers haven’t faced the same kind of margin calls, but they stand to suffer painful losses. As interest rates fell, they shifted to real income-earning assets like commercial real estate. The value of commercial real estate investment companies on the US stock market has fallen by 35%, about the same amount as the Nasdaq.

If that’s any indication, the $20 trillion value of the commercial real estate market has lost about $7 trillion this year, in addition to losses of nearly 20% on corporate bond and stock portfolios. Stocks and bonds, the largest components of pension portfolios, are down about 20% during 2022, depending on which survey of pension fund asset allocation you believe – the average US pension has probably lost more than 20% of its asset value this year.

Indeed, pensions don’t even need to have a near-death experience like in the UK: if the value of underlying assets drops enough, the forced selling will begin sooner or later. And once the capitulation really kicks in, followed closely by mass layoffs, only then will we find how determined the Rockefeller’s FED is to blow up the US economy and markets, in order to save, and hang onto, their faltering global dollar empire.

“Markets stop panicking when central banks start panicking.” And central banks are starting to panic more with every passing day. First it was the BOJ, then the BOE and now, for the second week in a row, it’s Switzerland’s turn.

The last week of September, after the (first) panicked pivot by the BOE, when global markets were in free-fall, and with the dollar soaring to new all-time highs every day – the Fed had to make some pre-emptive announcement on USD FX swap lines, if only to reassure global markets that amid this historic, US dollar short squeeze, at least someone can and will print as many as are needed to avoid systemic collapse.

So fast forward to October 5, when there still hasn’t been any formal announcement from the Fed, but ever so quietly the Fed shuttled $3.1 billion to the Swiss National Bank to cover an emergency dollar shortfall.

Many European, Asian and other large international banks are tied into the dollar system. This requires these banks to hold large dollar reserves to meet the needs of their clients. In a world of dollar shortages, and scarce dollars (as most dollars have fled to New York to earn higher rates,), what happens when these banks need dollars? That’s when the US FED lends these central banks enough dollars to meet their short-term dollar needs. Remarkably, this was the first time the Fed sent dollars to the SNB this year, and the first time the Fed used the swap line in size (besides a token amount to the ECB every now and then)! But it certainly won’t be the last time – as we have warned, expect far wider use of Fed swap line usage as the world chokes on the global dollar shortage – and sure enough- overnight, the Fed announced that as of Thursday it doubled the size of its USD swap with the world’s most pristine economy and its central bank, the Swiss National Bank, sending some $6.27 billion to avoid an emergency funding crunch.

Fed has pulled the plug

With the 0.75% Fed rate hike, largest in almost 30 years, and promise of more to come, the US central bank has now guaranteed a collapse of not merely the US debt bubble, but also much of the post-2008 global debt of $303 trillion. Rising interest rates after almost 15 years mean collapsing bond values. Bonds, not stocks, are the heart of the global financial system.

US mortgage rates have now doubled in just 5 months to above 6%, and home sales were already plunging before the latest rate hike. US corporations took on record debt owing to the years of ultra-low rates. Some 70% of that debt is rated just above “junk” status. That corporate non-financial debt totaled $9 trillion in 2006. Today it exceeds $18 trillion. Now a large number of those marginal companies will not be able to rollover the old debt with new, and bankruptcies will follow in coming months. The cosmetics giant Revlon just declared bankruptcy.

The highly-speculative, unregulated Crypto market, led by Bitcoin, is collapsing as investors realize there is no bailout there. Last November the Crypto world had a $3 trillion valuation. Today it is less than half, and with more collapse underway. Even before the latest Fed rate hike the stock value of the US megabanks had lost some $300 billion. Now with stock market further panic selling guaranteed as a global economic collapse grows, those banks are pre-programmed for a new severe bank crisis over the coming months.

The Federal Government will now find its interest cost of carrying a record $30 trillion in Federal debt far more costly. Unlike the 1930s Great Depression when Federal debt was near nothing, today the Government, especially since the Biden budget measures, is at the limits. The US is becoming a Third World economy. If the Fed no longer buys trillions of US debt, who will? China? Japan? Not likely.

Deleveraging the Bubble

With the Fed now imposing a Quantitative Tightening, withdrawing tens of billions in bonds and other assets monthly, as well as raising key interest rates, (a frantic process of trying to hold up the confidence factor )financial markets have begun a deleveraging. It will likely be jerky, as the key players within the networks of power of these 2 families, seek to control the meltdown for their purposes. But the direction is clear. By late last year investors had borrowed almost $1 trillion in margin debt to buy stocks. That was in a rising market. Now the opposite holds, and margin borrowers are forced to give more collateral or sell their stocks to avoid default. That feeds the coming meltdown. With collapse of both stocks and bonds in coming months, there goes the private retirement savings of tens of millions of Americans. Credit card, auto loans and other consumer debt in the USA has ballooned in the past decade to a record $4.3 trillion at end of 2021. Now interest rates on that debt, especially credit card, will jump from an already high 16%. Defaults on those credit loans will skyrocket.

And, many corporations managed to survive by borrowing money at ultra-low rates. Now, interest payments on this debt have jumped by 400%, with no end in sight. The result will be an increase in bankruptcies and rising unemployment.

Outside the US what we will see now, as the Swiss National Bank, Bank of England and even ECB are forced to follow the Fed raising rates, is the global snowballing of defaults, bankruptcies, amid a soaring inflation which the central bank interest rates have no power to control. About 27% of global nonfinancial corporate debt is held by Chinese companies, estimated at $23 trillion. Another $32 trillion corporate debt is held by US and EU companies. Now China is in the midst of its worst economic crisis since 30 years and little sign of recovery. With the USA, China’s largest customer, going into an economic depression, China’s crisis can only worsen. That will not be good for the world economy.

Italy, with a national debt of $3.2 trillion, has a debt-to-GDP of 150%. Only ECB negative interest rates have kept that from exploding in a new banking crisis. Now that explosion is pre-programmed despite soothing words from the ECB. Japan, with a 260% debt level is the worst of all industrial nations, and is in a trap of zero rates with more than $7.5 trillion public debt. The yen is now falling seriously, and destabilizing all of Asia.

The heart of the world financial system, contrary to popular belief, is not stock markets. It is bond markets—government, corporate and agency bonds. This bond market has been losing value as inflation has soared and interest rates have risen since 2021 in the USA and EU. Globally this comprises some $250 trillion in asset value a sum that, with every FED interest rise, loses more value.

As bond prices fall, the value of bank capital falls. The most exposed to such a loss of value are major French banks along with Deutsche Bank in the EU, along with the largest Japanese banks. US banks like JP MorganChase are believed to be only slightly less exposed to a major bond crash. Much of their risk is hidden in off-balance sheet derivatives and such. However, unlike in 2008, today central banks can’t rerun another decade of zero interest rates and QE. This time, as insiders like ex-Bank of England head Mark Carney noted three years ago, the crisis will be used to force the world to accept a new Central Bank Digital Currency, a world where all money will be centrally issued and controlled. This is also what Davos WEF people mean by their Great Reset. It will not be good. A Global Planned Financial Tsunami Has Just Begun.

“Markets stop panicking when central banks start panicking.”

Well, in what may be the best news to shell-shocked bulls after the worst September and worst Q3 in generations, in a harrowing year for markets, central banks are starting to panic. First it was the BOJ, then the BOE and now, it’s Switzerland’s turn.

The next logical question obviously is: why does Switzerland suddenly have a financial institution needing $6 billion in cheap (3.33%) overnightfunding. We don’t know the answer, but have a pretty good idea of who the culprit may be – the relentless dollar could forge a path to the next market upheaval.

Here’s how it could happen: Foreigners have snapped up dollar-denominated assets for higher yields, safety, and a brighter earnings outlook than most markets.A big chunk of those purchases are hedged back into local currencies such as the euro and the yen through the derivatives market and it involves shorting the dollar. When the contracts roll, investors have to pay up if the dollar moves higher. That means they may have to sell assets elsewhere to cover the loss. When the central bank steps on the brakes, something goes through the windshield. The cost of financing has gone up and it will create tension in the system. The market probably saw some of that pressure already: investment-grade credit spreads spiked close to 20 basis points toward the end of September. That’s coincidental with a lot of currency hedges rolling over at the end of the third quarter, he said — and it may be just “the tip of an iceberg.” And the fact that the Fed is already quietly shuttling billions of dollars to various central banks to plug dollar overnight funding holes, confirms that the rising dollar has already done just that.

But, the main danger lies just under the surface, and it is one where no one talks about it. This is the world of derivatives. The elephant in the room are the ticking time bomb of derivative losses by these international banks.

I have extracted a few paragraphs from a previous article on this site called: “FINANCE: DERIVATIVES & THE IMPLODING FINANCIAL SYSTEM, dated 25th October, 2018. It would be of great help if you were to read this article in full. https://behindthenews.co.za/finance-derivatives-and-the-imploding-financial-system/

Most people don’t understand what derivatives are. Unlike stocks and bonds, a derivative is not an investment in anything real. Rather, a derivative is a legal bet on the future value or performance of something else. Just as one can bet on the horse, or the outcome of a sports game, financiers in London and New York make multi-billion dollar bets on how interest rates, foreign exchange rates, and share prices will perform in the future; or on what credit instruments are likely to default.

A financial derivative is an instrument based on or “derived” from underlying assets such as shares, bonds, commodities or currencies. In general, it is an obligation to buy or sell the underlying asset at an agreed price and time in the future. Since it usually takes only a small down payment (the margin or premium) to purchase such an obligation, any movement in the value of the underlying asset above or below the agreed price can produce immense profits or losses relative to the original down payment.

Financial derivatives have grown from a standing start in the late 1980s to a $2 quadrillion industry by 2021. The world’s GNP stands at about $70 trillion; this is 30 times more than the global GNP figure. We are talking about an amount of money that is absolutely mind-blowing.

Derivatives are not bad in themselves. Used properly and wisely, they are an undoubted benefit. It is when they are used improperly and unwisely that they become the equivalent of a bomb. Think of derivatives as a loaded gun. You can use it in self-defense or murder. Unfortunately, the temptations to use it for the latter purpose are immense.

This worries many people in the finance industry. What concerns them is the growing fragility of the financial system they have created. Derivatives have built interconnections between markets that never existed 30 years ago; they have woven international finance into a single fantastically tight and complex tapestry, yet the fabric seems thinner than ever. Says a former central banker who has had to grapple with the reality of bank collapses and the threat of systemic financial failure says “derivatives have the potential to create an unprecedented financial disaster”.

It could happen. If it does, it will almost certainly be in a way that no one has foreseen. It may be triggered by an extraordinary event that nobody in their wildest dreams had imagined. But more likely it will involve nothing more remarkable than the sort of problems that regularly crop up on the markets, only this time the particular combination of events will be so unusual, so unexpected, the results will be lethal.

In times of crisis, the financial system reacts in unpredictable ways. The more suddenly the crisis strikes, the worse the trauma is likely to be. Investors, caught off-guard and protecting their own individual interests, will react in all the wrong ways ; governments and financial regulators will be confused and paralyzed, perhaps making mistakes that worsen the situation ; the crisis will spread like lightning across countries and markets, faster than anyone can control until suddenly a local problem has become a global disaster. But not all such blunders become public knowledge. As everyone knows, banking is to a great extent a confidence trick. Banks only last as long as their depositors believe that their deposits are safe, so bankers see it as a duty to reassure the public even if that means misleading them. It is normally not until a bank is in direct trouble that the public ever gets to hear about it.

Just because the financial system did not crack in 2008, does not mean that a somewhat bigger shock could not create the ultimate financial nightmare – what the bankers call systemic risk – because if we can be sure of anything about the financial system is that something will eventually go wrong. It is not a question of if, but when. These past financial eruptions are but a precursor to the “big one”, a reverse-leverage disintegration of the entire financial system in a matter of days, or hours.

The Crash – It’s After-Effects

Today, (October 2022), we have the biggest financial bubble in history. Every financial institution in the world is bankrupt, or close to it. Global financial turnover is about $6 trillion a day, with obligations based in this financial system. Most of these obligations are invisible, but they make themselves visible when somebody tries to collect. It’s like a gambling debt. It’s only when the guy comes to collect it, then it becomes visible. Only then is the family aware of what’s going on.

In a chain reaction, we find people rushing to try and collect, not because Wall Street is collapsing, but because the derivative market is collapsing. Banks and speculators are trying to save themselves. Within a period of as short as 3 working days, the banks will not only collapse, but also the entire financial system will vaporize. It will be an implosion, because of the ratio of unpayable debts coming due at once, hitting the virtually non-existent margin of assets to cover it. For example: Look at your wallet. How much of your money is in electronic form? How much of your money is actually cash? How many dollars/euros/pounds do you withdraw from the bank, and deposit – money- as opposed to electronic deposits and electronic withdrawals? How much credit that you rely upon, comes in the form of electronic credit as opposed to cash? What does that electronic credit mean? It means you have a banking institution, which guarantees the conversion of that electronic credit into money. Now, what happens if that institution suddenly, no longer functions? You are there with a card; it is no good.

Now, what happens in about 3 or 5 days’ time at the local supermarket? They are functioning on electronic money. What happens when the current stock of groceries runs out – and there will be a rush for groceries? What happens? They can’t get more groceries. The supply chain breaks down. Institutions break down. In modern economies, people do not realize how vulnerable they are. We no longer have local farms. We depend upon credit, especially electronic credit, and local stores and we get by through the week, largely on the basis of electronic credit. What happens if that system of electronic credit breaks down? Then you actually get conditions of mass starvation throughout the world. The whole system of commerce comes to a standstill. And that is what we are facing, unless something is done to deal with that.

The weakest part of the system lies in the interbank payment system (details of this will be explained in another issue) that, in turn, depends upon the extent of losses incurred by the major players in the market.

JP Morgan Chase

To give an example: JP Morgan Chase has an equity capital of $ 178 billion; assets (loans) of $2.1 trillion. And a derivative book of $78.7 trillion! This was as of December 31, 2010. That’s 12 years ago. In other words, its equity capital is equal to .24% of its derivative book. A loss equivalent to just .25% of its derivative portfolio would wipe out JP Morgan Chase’s entire equity! The ratios are slightly better for the other large international banks. That tiny margin between existence and disintegration is a dominant feature of the international financial system today, and this is what has financiers, the regulators, and the politicians terrified. One false move and poof! The whole thing blows. To sum up: the huge mass of financial values in the world economy has the form of an inverted pyramid. On the bottom of the pyramid, we have the actual production of material goods. Above that, is the commercial trading in commodities, and real services. Above that, we have the complex, interconnected structure of debt, stocks, currency trading, commodities futures, and so on. Finally, at the top, we have derivatives and other forms of purely fictitious capital.

This strange object is growing in a very unbalanced way: the upper layers – starting with derivatives – grow much faster than the lower layers. But, what is happening at the very thin base of the pyramid, which represents the real, physical economy? Actually, it is not growing at all. In fact, the world’s physical economy has been stagnating, even declining, since the 1970s. Looking at the situation for the world as a whole, we can see that the portion of physical output flowing back into agriculture, industry, and infrastructure has been decreasing. At the same time, fictitious capital is growing at an accelerating rate. What is actually happening, is that the productive base of the world economy is being ‘sucked to death’ by the pyramid –shaped financial bubble. This is most clearly seen by the effect of the massive debt accumulation, which is causing farms and industries, and even entire governments, to shut down. The whole financial bubble depends, directly and indirectly, on “squeezing” increasing amounts of income flows from the material base of the world economy.

This is the background for the call of globalization and free trade by New York and London. When nations around the world subscribe to these policies, they leave their economies wide open to be looted by these two networks. Both London and New York are desperately trying to prop up the financial bubble, and it needed to “open” the economies of various nations, in order to facilitate its looting of these economies. When these nations resist, their leaders are destabilized by “political scandals”, or worse, when the entire nation itself is targeted for destabilization, through wars, coups, color revolutions, etc.

America is very close to bankruptcy. It survives only by the tyrannical use of raw political, financial, and military power, to exact tribute from much of the rest of an already looted world. The world has been pumping roughly $3 billion per day into the US, in order to keep America going. Now, they have become very tired. The current economic and financial crisis is not something which might happen. It is something that is already underway. What we do not know at this stage is that when the already existing, hopeless bankruptcy of the system will explode into the streets – is whether this will occur as a single event, or as a cumulative effect of a chain-reaction series of crisis, ricocheting around the world.

Whenever these two networks find their economic, financial, and political systems threatened, they react with VIOLENCE. In other words, when they cannot control the world by means of their financial and economic systems, they use the desperate action of the FIST to destroy and crush anybody who might be in their way.

We are now in such a period. We have the worst finance and monetary crisis in modern history. While the financial elite are bailing out of the stock markets, fools like us are persuaded to buy yet more shares in the same markets. All the largest bank groups are technically bankrupt. The situation in Europe is even worse. Of the estimated 50 trillion Euros of loans on its books, almost 30%, or 15 Trillion worth, is beyond recovery. This 15 trillion is multiple times more than the capital base of the European banks. And most of the largest European banks are in the Rothschild orbit.

From this point alone, we can now understand why the British are the main cheerleaders in the current war. They need Russia destroyed and taken over, in order to save their financial empires. The Rothschild desperation is becoming hysterical- as can be seen by the actions of the political class in London and Brussels. Europe is beyond broke. Things are so bad that they struggle just to fulfill their pledges to aid Ukraine financially. Only about 15% of the total pledged to Ukraine from London and the EU has been sent to Ukraine!

With this in mind, when one hears the EU saying that they are going to steal the Russian funds frozen in Europe, you can understand why. Calls for this will become deafening by year-end.

With every passing day, the demands for austerity coming from the financiers of the Anglo-American empire grow louder. Governments worldwide are being told that they must slash their budgets, cut their services, and shred their social safety nets, and cast their populations to the wolves, all in the name of “fiscal responsibility.” “All available resources must be funneled to us,” the financiers shriek. “We need the money, and the people must fend for themselves!”

At the same time, the financier networks of the 2 families that are making these inhuman demands are continuing to loot the planet through a variety of open and hidden bailout schemes, currency manipulations, and derivatives, plus outright theft of assets of those who are not with the 2 families- in short, these bastards continue to steal us all blind – destroying the basis for our very existence.

The Crash Begins

The entire trans-Atlantic financial crash is in full swing, and this collapse is gaining more and more momentum. Faced with indebtedness and derivatives exposures amounting to the trillions, Wall Street and London have only two cards up their sleeve: further money printing and the theft of depositors’ funds, and expropriation of investors bonds and stockholders. This can only be described as criminal. The more this crash expands the more human lives it will cost. Under this new bail-in policy now being implemented , everything you and your family may have – savings, pensions, food, health care, jobs, homes, everything – will be seized in the name of protecting the criminal financial system which created that speculative bubble. This is what is predicted for 2023; massive sacrifice of savings and jobs to prop up a bankrupt global financial system. On this point, please read our article. Called “ICE-NINE- How the Elites are planning to steal your money, dated 10 February 2018, https://behindthenews.co.za/ice-nine-how-the-elites-plan-to-steal-your-money-the-global-financial-lockdown/

The actual root of the problem is that people fell for the lie that money is actual wealth, and an entire financial system has been built on that lie. But, money is not something which has a self-evident value. Value depends upon the creative powers of mankind, to make better the conditions of life of mankind.

As the system is tearing apart, other countries may try to insulate themselves from this by embracing capital controls. The dollar has no peers. But the system that it anchors is cracking. Panic among Wall Street and City of London bankers is evident just barely below the surface. When financial markets are crashing, wars inevitably follow. That is even more reason to keep a close eye on events in Ukraine and Syria. As the competing nations try to grab the energy resources of the area, all it would take is a spark to detonate World War Three!

In our next article, we will do an update on the war in Ukraine, and for the conflict within Syria. These 2 conflicts represent 2 of the 3 ignition points that the 2 families are trying to blow up. The 3rd ignition point is Eastern Eurasia – the China/Japan/Korea triangle. And, in all 3 areas mentioned, the 2 families are hurriedly preparing for an escalation. Will it go nuclear? The chances are high- for one simple reason. The heads of the 2 families have come to a decision: “I would rather blow the planet up, than lose my Empire!”

At the current rate the euro is dying, most likely that, in the next year, within the EU and the UK, we will see increasing debt defaults of municipalities, governments and companies. This will be followed, within a short time, in the US itself. To add to the panic on Wall Street and the City of London, MBS is pivoting East. Were this to happen, then it is the ultimate game-changer for Western finance.

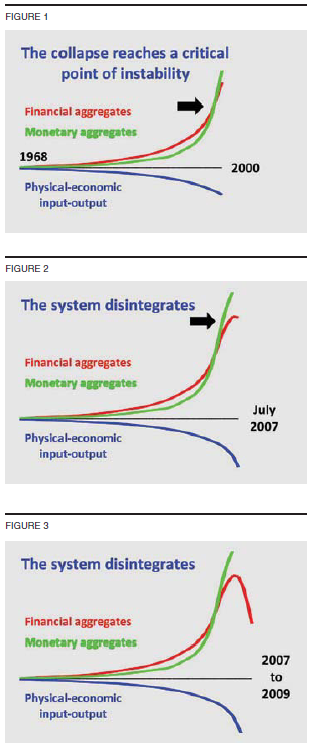

Below, is the famous TRIPLE CURVE FUNCTION, authored by world renowned economist Lyndon LaRouche Jnr. For further reference on this subject of physical economy, visit the EIR website, via LaRouchepub.com.

That’s is the position the world was in on last day of October 2022.

I’m a great admirer of this site of utmost importance. If the authors would pen an article called “Essential reading: books, articles etc”, it would help greatly to the readers.