The story continues from Part 1. Back to China……

3 Comparison between the World’s Two Largest Economies

A thermodynamic audit of China vs. the US and measuring civilizational rank in the 21st Century

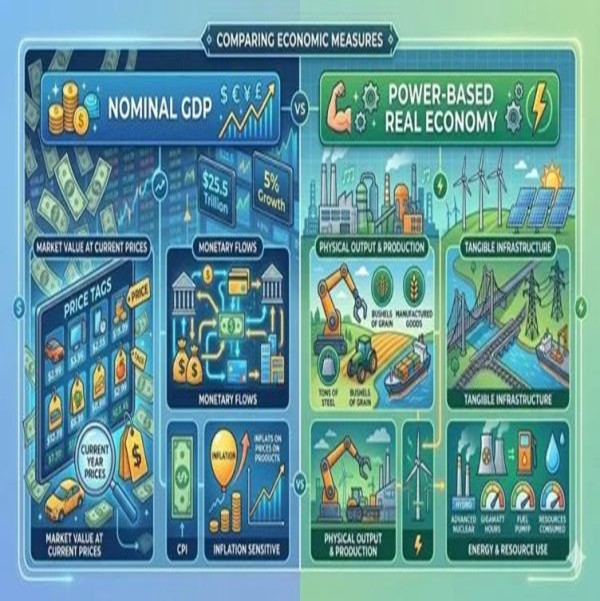

There are many ways to compare size of economies. The most common method is the nominal GDP, based on exchange rates of different currencies. By this standard, the US has the largest economy of the world at US$30.5 trillion in 2025, approximately 50% bigger than China’s US$19.4 trillion. Another popular measure is the Purchasing Power Parity GDP (PPP), which adjusts for price levels and the local cost of living. By this measurement, the size of China’s economy is around US$41 trillion vs. the US’s US$31 trillion. Economists also use the output of various sectors to compare different economies at a more granular level. For example, China produces 35 million cars in 2025 vs. 10 million in the US. China produces 960 million tons of steel and 1.7 billion tons of cement vs. 82 million tons of steel and 86 million tons of cement in the US. China has roughly 60% global shipping market vs. the US’s 0.1%. On the other hand, the FIRE sector (finance, insurance and real estate) in the US generated GDP of $6 trillion in 2025 vs. China’s $2.5 trillion. US healthcare sector generated $5.3 trillion GDP vs. China’s $1 trillion. Clearly, the structure of the two economies is vastly different and doesn’t lend itself to easy comparisons.

Energy Production and Consumption as the Metric for Economic Output

There has been a lot of recent interest in the role of energy in the new age of artificial intelligence. All of sudden, we are hearing from Silicon Valley highfliers and Wall Street pundits that energy is critical in the AI race and who produces more energy will determine who rules in the age of AI. Energy is now considered a proxy of national power. In fact, this is hardly a novel idea. In 1964, a Russian scientist named Nikolai Kardashev created the Kardashev Scale to measure how advanced a planetary civilization is. Instead of looking at how intelligent or creative a civilization is, the Kardashev Scale looks at one thing: how much energy they can produce and use. The more energy a civilization can control, the higher they rank on the scale.

China is the planet’s largest energy and power producer. It produces approximately 33% of global electricity versus 14% by the US, according to the International Energy Agency (IEA). China’s total installed power capacity has reached approximately 3,890 gigawatts (GW), nearly 3 times of the US’s total power base of 1,373 GW. China surpassed the US in electricity production and consumption since 2011. The amount of new power capacity China has built just since 2021 is larger than the entire power grid of the US. In terms of power mix, China has built the world’s largest renewable energy system. China’s total renewable capacity alone (1,800+ GW) is larger than the entire U.S. electrical capacity. China is also expanding its green energy production faster than any country in history, installing more clean power capacity than the rest of the world combined. China accounts for over 37% to 40% of all global electricity generated from solar and wind. Benefiting from massive infrastructure like the Three Gorges Dam, China produces roughly 30% of all global hydro-electricity. China manufactures 92% of the world’s solar modules and 82% of the world’s wind turbines. There are 36 nuclear reactors under construction in China, equal to the rest of the world combined. China added a total of 543 gigawatts (GW) in new power capacity across all energy sources in 2025, 60% of which from renewable energy. The US added 64 GW in 2025, driven by the demand for AI data centers. For reference, the entire installed electricity capacity of Germany, the largest in Europe, is 290 GW. If electricity is the “pulse” of a real economy, then by 2026, China has become a different species of superpower. In 2025, China’s annual power consumption had surpassed 10.4 trillion kWh —a staggering milestone that makes China the first nation in history to break the 10-trillion mark.

To understand the scale of this physical economy, consider these comparisons:

- Total output: China’s power grid is now roughly 2.5 to 3 times larger than that of the US

- Growth gap: In 2025 alone, China added 540 GW of new generation capacity. This annual addition is nearly half of the total installed capacity of the entire US grid

- “New Three” Surge: the growth in China’s power demand is driven by what it calls the “New Three” industries: Electric Vehicles (EVs), Lithium-ion batteries, and Solar PV.

In 2025, electricity used just for EV manufacturing and wind equipment surged by 20% and 30% respectively. While the U.S. celebrates “energy efficiency,” China is practicing “energy intensity. “In a Kardashev sense, China is behaving like a civilization attempting to leap to a higher state of complexity, while the US is behaving like one attempting to maintain its current state with fewer calories. It is clear the US is focused on militarily confronting China in Taiwan. China’s military advancement is forcing the US to spend huge amounts of money to get ready for a war:

- The recently announced F-47 sixth generation fighter program

- Developing hypersonic missile technology to catch with China and Russia

- Developing hypersonic defense

- Preparing for space warfare such as the orbital carrier concept from Gravitics

- Upgrading naval ship building for both surface vessels and submarines

- Investing in large scale swarming drones

- Military AI and robotics

- Upgrading nuclear arsenal

- Fortressing Guam for potential Chinese attacks

- Building and fortifying military bases in Japan and the Philippines

The for-profit US military industrial complex will pile in to maximize costs. Those include not only the 5 oligarchs monopolizing arms sales today but new entrants peddling overpriced new solutions such as Anduril and SpaceX. Expect to see more no-bids contracts like the Boeing F-47 program. As China currently spends less than 1.5% GDP on defense vis-a-vis 3.5% for the US and 2% global average, China can easily afford to up the ante and trigger further military spending from the US. Just as the US bankrupted the USSR to win the Cold war, history is repeating itself and China will force the US to spend its way to defeat. Sun Tzu defined the best war strategy is to win without fighting.

The Hamilton Index: Measuring Industrial Competitiveness of Nations

The Hamilton Index is an economic scorecard that measures how well countries compete against each other in 10 strategically important, high-tech industries. Created by the Washington-based a major economic think tank, the index tracks industries that are critical for both national security and global trade. It is named after Alexander Hamilton, the first US Treasury Secretary, who championed the idea of building a strong national manufacturing base. The index acts as a health check for a country’s industrial backbone. Rather than looking at regular construction or simple retail, the Hamilton Index aggregates global market shares and value-added output for 10 critical industries including:

- Computers, electronics, and microchips

- IT and software services

- Pharmaceuticals

- Motor vehicles

- Electrical equipment such as transformers and turbines

- Machinery and equipment

- Chemicals

- Basic metals and Fabricated metals

- Other transport equipment (like aerospace and trains)

The index does not just rank countries by who is the biggest. Instead, it uses a math formula called a Location Quotient (LQ) to see how heavily a country focuses its economy on these technologies compared to the rest of the world. LQ of 1.0 means a country is perfectly on par with the global average. LQ above 1.0 suggests the country is hyper-specialized and “over-performing” in high-tech manufacturing. LQ below 1.0 means the country is lagging behind and relies too heavily on other fields such as agriculture, finance, or basic tourism.

The Hamilton Index findings highlight a massive shift in global power:

- China is Dominating: China has shot past the global average with an LQ of 1.36, meaning its economy is 36% more concentrated in high-tech industries than the world average. China commands over 30% of the entire world’s output across these 10 fields and leads the globe in 7 out of 10 categories.

- The US is Lagging: the US falls below the global average with an LQ of 0.88. Even though the US has massive software and tech companies, its actual manufacturing base for hardware and electronics has shrunk. To match China’s tech intensity, the U.S. would need to add $1.5 trillion in advanced manufacturing output annually.

Real Economy vs. Nominal Illusion

For over a century, the global hierarchy has been dictated by a single, undisputed metric: Gross Domestic Product (GDP). We have been taught that the nation with the highest market value of goods and services is the most advanced. However, in the mid-2020s, a fundamental crisis of measurement has emerged. As the US and China diverge in their economic strategies—one prioritizing “bits and financial flows” and the other “atoms and energy throughput”—the traditional GDP metric is failing to capture the true distribution of power. If we apply the lens of the Kardashev Scale, which ranks civilizations by their ability to harness energy, and the Hamilton Index, which tracks dominance in physical manufacturing, a different reality emerges. By these thermodynamic standards, the “real” economy is shifting away from the West, revealing that nominal wealth may be a cover for physical stagnation. In 2026, the United States remains the world’s largest economy by nominal GDP. Yet, a forensic audit of these numbers reveals a startling lack of physical metabolism. Approximately 80% of US GDP is derived from the service sector—a broad category that includes high-value activities like software engineering and medical research, but is dominated by financial services, insurance, and “imputed rent” (the theoretical value homeowners pay themselves). These activities are “energy-light.” A law firm in Washington D.C. can generate $500 million in annual revenue while consuming less electricity than a single medium-sized injection-molding factory in Guangdong. In the nominal world, the law firm is “bigger.” In the physical world, the factory is the true unit of civilizational power. The result is a decoupling of wealth from energy. While US GDP continues to grow at a modest 2–3%, its total electricity consumption has remained largely stagnant for two decades, hovering around 4.1 trillion kWh. This is the hallmark of a “Rentier Economy “—a system that grows by increasing the price of existing assets and services rather than by expanding its physical mastery over the environment.

The Mastery of Atoms

The divergence is most visible in the Hamilton Index. China produces closely to 1/3 of global output in the 10 critical industries and 36% above global average industrial density. The US is 12% under global average in industrial density. For it to match China’s level of industrial intensity relative to its economy, the US would need to increase its industrial output by $1.5 trillion annually. This “Real Economy” gap is why China produces 52% of the world’s steel, compared to the US share of 4.4%. Together with solar panels and EVs, these are not just “commodities”; they are the primary building blocks of a Type 1 civilization. You cannot build a Dyson sphere or even a national high-speed rail network with “financial services.” You build them with steel, silicon, and massive amounts of electricity. Humanity currently sits at approximately Type 0.73 on the Kardashev Scale. To reach Type 1 —planetary mastery—we must increase our energy harnessing by orders of magnitude. China is attempting a “Brute Force” ascent. By leading the world in 4th generation nuclear reactors and breaking records in fusion plasma duration it is building the hardware of a Type 1 civilization. The US is attempting an “Algorithmic” ascent. It is betting that superior software (AI) and financial efficiency will allow it to lead without needing the same physical footprint. However, history suggests that “bits” always follow “atoms.” The British Empire was the master of global finance (the bits) in the 19th century, but it was overtaken by the US because the US mastered the internal combustion engine, the electric grids, and mass manufacturing (the atoms). If you define the “Real Economy” as the ability to transform the physical world, then the audit is clear: China’s real economy is significantly larger and more advanced than that of the United States, regardless what the GDP numbers tell you. While the US remains the master of the “nominal” world—holding the reserve currency and the dominant stock indices—these are social constructs that can vanish in a crisis. Kilowatt-hours, steel tonnage, and satellite-captured night-time luminosity are not social constructs. They are thermodynamic facts. As we head toward the mid-21st century, the nation that treats energy as its primary currency will be the one that dictates the terms of human advancement. The US and the broader West must decide if it is content to be a high-priced “boutique” civilization, or if it will return to the hard, energy-intensive work of building the future. In the end, the universe does not care about your GDP; it only cares about your power.

4 The AI Bubble

All data centers in the US fall under the authorityofthe Military Installation Development Authority (The MIDA). MIDA effectively functions as a local government within the areas it develops. While developments generate property and sales tax revenue that the agency then uses for future projects — the state and county provide tax rebates back to the developer. And MIDA — not the county or municipality — controls land use and planning decisions within the areas. The one sector where the US is rediscovering the importance of energy is artificial intelligence. In 2026, data centers have officially hit a wall: they now consume 6% of all US electricity, a figure that has triggered political pushback and grid stability warnings. The AI boom is proof that even the “digital” economy eventually hits a physical limit. The land alone for these data centers is in the billions with military intelligence costs considered “classified”.

The purpose? Surveillance.

As explained in previous articles, the “powers-that-be “- headed by the Rockefeller family, have decided to implement several programs that they have been working on for years, and in some cases, decades. That is a full-blown surveillance and control of human populations. This has taken on an urgency in recent years due to the imploding financial system, and a weakening American military posture. Both deadly to the aims of total global full-spectrum domination. The family is in a race against time.

Here are some quotes from Brzezinski

He wrote and published a book, “Between Two Ages – America’s role in the technetronic Era “in July 1970.This bookexamines the impact of the technological revolution on the social and political values, institutions and directions of the U.S. and other industrial nations. From this, we can extrapolate the family’s long-term thinking and planning. Remember, even though this book was published in 1970, these discussions were ongoing prior to the publication.

- I foresee a time when we shall have the means and therefore, inevitably, the temptation to manipulate the behavior and intellectual functioning of all the people through environmental and biochemical manipulation of the brain.

- In the technetronic society the trend would seem to be towards the aggregation of the individual support of millions of uncoordinated citizens, easily within the reach of magnetic and attractive personalities exploiting the latest communications techniques to manipulate emotions and control reason.

- Technology will make available to the leaders of major nations, techniques for conducting secret warfare, of which only a bare minimum of the security forces need be appraised…techniques of weather modification could be employed to produce prolonged periods of drought or storm.

- technetronic era involves the gradual appearance of a more controlled society. Such a society would be dominated by an elite, unrestrained by traditional values. Soon it will be possible to assert almost continuous surveillance over every citizen and maintain up-to-date complete files containing even the most personal information about the citizen. These files will be subject to instantaneous retrieval by the authorities.

- People, governments and economies of all nations must serve the needs of multinational banks and corporations.

- Shortly, the public will be unable to reason or think for themselves. They’ll only be able to parrot the information they’ve been given on the previous night’s news.

- We have a large public that is very ignorant about public affairs and very susceptible to simplistic slogans by candidates who appear out of nowhere, have no track record, but mouth appealing slogans

- It is that [American exceptionalism] is a reaction to the inability of people to understand global complexity or important issues like American energy dependency. Therefore, they search for simplistic sources of comfort and clarity. And the people that they are now selecting to be, so to speak, the spokespersons of their anxieties are, in most cases, stunningly ignorant.

- in the so-called modern world, the intellect has been dumbed down and marketed. In today’s America, the box has become the paradigm, the source of what is real and acceptable.

- Another threat, less overt but no less basic, confronts liberal democracy. More directly linked to the impact of technology, it involves the gradual appearance of a more controlled and directed society. Such a society would be dominated by an elite whose claim to political power would rest on allegedly superior scientific knowhow. Unhindered by the restraints of traditional liberal values, this elite would not hesitate to achieve its political ends by using the latest modern techniques for influencing public behavior and keeping society under close surveillance and control. Under such circumstances, the scientific and technological momentum of the country would not be reversed but would actually feed on the situation it exploits.

* Persisting social crisis, the emergence of a charismatic personality, and the exploitation of mass media to obtain public confidence would be the steppingstones in the piecemeal transformation of the United States into a highly controlled society. - National sovereignty is no longer a viable concept.

- The nation state as a fundamental unit of man’s organized life has ceased to be the principal creative force: International banks and multinational corporations are acting and planning in terms that are far in advance of the political concepts of the nation-state.

- People, governments and economies of all nations must serve the needs of multinational banks and corporations

So, there you have it folks. From the mouthpiece of a key Rockefeller advisor, who would serve Carter as his National Security Advisor. Need anything more be said! Let’s study the example of just 1 data center: –

Camp David Data Center in Utah

One such data center is owned by the NSA and is located at Camp Williams, Utah. Perspective: The Camp David data center is 100,000 sq mts (about 25 acres). 10 % of this is designated mission critical Tier III, while the remainder is designated technical support. Completed in 2014, the 20-building complex includes water treatment facilities, chiller plants, electric substation, fire pump house, warehouse, vehicle inspection facility, visitor control center, and 60 diesel-fueled emergency standby generators and fuel facility for a 3-day 100% power backup capability. The electricity cost for Camp Williams data center is $70 million; maintenance is another $20 million; water usage is 7 million liters daily. It is built on a desert.A single high-end AI training cluster can require 100 MW of power—the equivalent of a small city. This is forcing the US to reconsider its “bits over atoms” strategy. For the first time in thirty years, US tech giants are investing directly in nuclear power (SMRs) because they have realized that intelligence is a function of energy.

Data centers has come under intensive backlash given the amount of water such a facility would consume. The revenue produced by the facility is tax revenue which will be absorbed by the Utah citizens in higher energy and water bills. Infrastructure fees are tacked on to water and electrical bills paid by consumers – data centers pay less and get rebates. So, taxpayers’ foot the bill for the data centers. Water rationing across the western slope is in high gear. Utah has 43 data centers with an additional seven in the works. At full capacity 9Gw, this one data center will use twice as much energy as the entire state now uses. MIDA effectively functions as a local government within the areas it develops. While developments generate property and sales tax revenue that the agency then uses for future projects — the state and county provide tax rebates back to the developer. And MIDA — not the county or municipality — controls land use and planning decisions within the areas. Adding to the problem – Colorado has 60 data centers. There are 1500 data centers planned for the US including the above.We currently have roughly 650. Already tapping out our energy, electric and water grid. Humans will have to leave to support the robots. The impact is phenomenal. These data centers are upsetting the neighbors of these places. Their water and power bills are increasing. Not only that, we find that electricity costs make these data centers not as profitable as many thought. In China, electricity costs are one-sixth of the US. This one fact alone puts the viability of centers into doubt.

The Hidden Costs of the Data Center Boom

The reality reveals that computing power, energy consumption, and high token usage make AI an exceptionally expensive line item. In fact, so expensive that businesses are shutting down use of AI as it is pricing them out of business. Nvidia’s Vice President of Applied Deep Learning publicly stated that compute costs for their AI engineering teams far surpass the actual cost of the employees’ salaries. An economic analysis by MIT found that AI is only cost-effective in about 23% of basic jobs; in the remaining 77%, keeping a human worker is the more economically viable option, making all those 5,000+ data centers ‘obsolete’ and the new ones being built a fictional storyline. It is called ‘token usage’ and small business owners are staring down bills as high as $113,000. Most users were burning $500 to $2,000 per month each. Microsoft is banning the use of AI by its engineers. The boom is going to bust after global spending reaching over $6.7 trillion. Across the board, tech companies claim that human employees are much more cost-effective. But current western scholarly education systems have failed to teach real world skills for engineers leaving 80% unemployable. Exasperating a problem that will become exponential as businesses scramble for humans to replace AI. It looks like we in the beginning stages of an AI bubble. Many companies were deepening their debt as they bought into the data center hype. Offloading AI means that debt remains with no value to offset it. When the value is gone, companies have to raise their pricing to mitigate the debt. And the inflation cycle ramps up rather quickly. The debt attached via bank loans could see bankruptcies rise as companies can’t afford the data costs much less the loans. The Pentagon, engaging in many of the largest data centers across the country, have yet to book or analyze the costs.

Although, on a brighter note, the economic realization may be a pushback for the launch of the ‘digital credit system’ as proposed by the networks of the 2 families. Building a global credit and financial system involves monumental outlays, including trillions in infrastructure and immense societal trade-offs. While the structure could be built in roughly three years, the integration would take another seven to ten years —variability being country-specific. According to Bloomberg, in 2026, half of all proposed data centers will face delays or cancellation. Why? Shortage of materials and supply chain delays. Components are not manufactured in the US so contractors need to buy from Canada, Mexico, South Korea and China. But Trump has created riffs with these countries hemorrhaging land loans, inflating building costs, while interest rates on loans eat up the remaining cash on hand, which is why corporations are looking into bond sales, bridge loans, and other means as time frames lag. With the realization that AI is cost-prohibitive, corporations scaling back will create a glut of outstanding loans against vacant land. Banks will look for bailouts. And the circle will stop short. Oracle has $100 billion in debt against an Abilene data center where clients are walking away. Outstanding debt has reached hundreds of billions with Morgan Stanley claiming the need for trillions in external funding in America alone.

Blackstone, which acquired QTS in 2021, is a major financier of data centers, with a portfolio of more than $150 billion of such assets around the world. Up until now, when it comes to real estate, Blackstone (in the Rockefeller orbit) was best known in recent years for dumping many of its trophy office properties – which in the aftermath of work from home never recovered their projected cash flow potential – at a loss. Now, it may be pulling a page from its old playbook, by calling in yet another commercial real estate segment: data centers. By end-June, Blackstone was selling its stakes in a trio of data centers across Northern Virginiafor $3.5 billion,cashing out of part of a bet it made less than three years ago. Digital Realty Trust would pay $1.2 billion of cash and offer $2.3 billion of its shares (which the PE giant has largely cashed in by now) to Blackstone funds; in exchange, the data center company will acquire Blackstone’s 80% interest in two 96-megawatt data centers in Manassas, Virginia, and a 50% interest in a 96-megawatt center in nearby Sterling. The digital ink is barely dry on its Virginia data center sales, and we learn that Blackstone’s QTS (QTS Realty Trust) is again quietly fading its AI exposure by walking away from plans to build its portion (which at this point is the only portion left after its partner already pulled out days ago) of a 2,100-acre data center campus in Virginia – which would house as many as 37 data-center buildings – handing a win to residents who fought for years to topple the project. QTS’s rapid growth has made it a poster child of how private equity has fueled the data center industry’s breakneck expansion. Those ambitions are colliding with public anxiety over strains to electricity grids and home prices from AI data centers.

As part of Wall Street’s broader push into data centers, investment has poured into Northern Virginia, which is considered the country’s largest data center market, and is better known as “data-center alley”. The retreat may be the final blow to Virginia’s “Digital Gateway” project, a mega site roughly twice the size of New York’s Central Park with city-sized power needs. The initiative was supposed to bring in some $100 billion in spending and create one of the world’s largest technology corridors. Not anymore. It’s a reminder of how tech firms’ race for the computing infrastructure to support AI advances is increasingly facing the same bottlenecks, from power shortages to supply crunches.

Organized opposition is mounting, forcing firms and developers to be more deliberate about where they choose to build. QTS’s pullout will now unleash even more powerful blowback nationwide against these unwanted developments. The increasingly bitter political and grassroots pushback against new data center construction explains why Blackstone has been getting cold feet just as the AI bubble is peaking, first selling existing data centers and now walking away from upcoming projects. A recent poll found that 7 in 10 Americans oppose constructing data centers for artificial intelligence. Blackstone, which manages more than $1.3 trillion, bills itself as the largest globalprovider of data centers, and also owns some of the utilities that power them. It acquired QTS in 2021 and bought Australian computing provider AirTrunk in 2024. In May, the firm held an initial public offering for Blackstone Digital Infrastructure Trust Inc., its data center acquisition vehicle, which aims to buy already built and leased properties benefiting from the artificial intelligence boom. And now that the protest movement knows how to push back against uninvited Wall Street occupants, thanks to the Blackstone capitulation, expect an exponential increase in legal (and other) attempts to hinder the rollout of data centers across the US, assuring that the AI super cycle, which is already years behind schedule with just half of the data centers meant to be built in progress and on time, will expect to see an avalanche of delays and cancellations assuring that the return on debt-funded capex will be even less as eventual launch dates gradually move ever further into the unknown future.

AI-replacing Human Labor

In the first quarter of 2026 American manufacturing output was up, hours were down, productivity was up. The factories are producing more, and the factories are using fewer hours of human labor to produce it. The wages paid to the humans no longer needed are no longer being paid. The factories do not need a recovery because the factories are not in a recession. The humans are. The labor share of US GDP is at 54.1% in the first quarter of 2026. This is the lowest reading since the Bureau of Labor Statistics began the series in 1947. In the year 2000 it was 63%. Three-fourths of the entire post-war decline happened between 2000 and 2016. The collapse is systemic. AI may be the accelerant, but it is not the only cause. There’s a name for this in the economic literature. It’s called productivity decoupling. It happens when productivity climbs and wages do not, when the gain accrues to capital and the labor share falls. The AI technology is good enough to displace workers but not good enough to create new tasks that humans are needed for. It cuts the labor demand without compensating with new demand. It’s good enough to replace the customer service agent, not good enough to make her a more valuable knowledge worker. Good enough to fire her. Not good enough to need her. China’s use of AI is being “democratized”, while in the US, AI is being militarized as a surveillance and control tool.

5 The Financial Equation

And the real contradiction—a post-productive economy trying to fund an AI future on mountains of debt—is never resolved. It is only papered over until the paper itself tears. Over the next two years, the AI/data center build-outwill cost $1.8 trillion in capital expenditure (capex), and hyperscaler capex alone to reach roughly $2 trillion over 2026-2027. And the tech sector has issued nearly 20% of all investment-grade bond issuance—double its historical share. The traditional bond market is saturated and the banks are tapped out. In June 2026, Blackstone stopped redemptions on its $79 billion private credit fund after requests hit 10% of the fund size. D.E. Shaw clients were informed that from January 2027, investors in its flagship hedge fund would need four years to fully exit—both firms citing the need to protect portfolios against “future crises.” The message couldn’t be clearer: the liquidity “is gone.” Meanwhile, Goldman Sachs handled $1.175 trillion in US equity supply in 2026—IPOs, secondaries, and lock-up expirations—just as hyperscalers like Meta post negative free cash flow and consider stock offerings because they can no longer fund their AI ambitions from operations.Add to this the approximately $900 billion in US corporate debt maturities coming due in 2026 (rising to nearly $1.5 trillion by 2028, and the picture is one of a market being squeezed from both sides: equity supply flooding in, debt needing refinancing at higher rates, and cash flow nowhere to be found. US firms have borrowed more than the real economy can ever even dream of repaying—and we can’t stop. Essentially, the growth of wealth is only simulated through credit creation. While this hyper-inflationary potential has so far been cynically exported to the neglected peripheries of the globalized world, it now constitutes a real threat for the “advanced” capitalist countries too—especially when we consider the ongoing grotesque expansion of the speculative sector.

The Contradiction

Capital today is caught in a contradiction it cannot resolve on its own terms. It requires endless growth to service debt and justify valuations, but the real economy is no longer capable of generating the surplus that endless growth demands. So, capital aggressively borrows from the future—it has done so for decades. It financializes with no end in sight. The Korean stock market is dangerously concentrated in three tech stocks: Samsung, SK Hynix, and Micron. The aborted labor strike reported in recent weeks was something like a dress rehearsal. Next time, the trigger might not be a labor dispute. It could be an earthquake, a fire, a power outage, a political crisis. But the chain reaction would be the same: Samsung halt → no HBM memory → Nvidia can’t ship chips → revenues miss → leveraged ETFs trigger sell vortex → private credit defaults → circular financing inverts → Nvidia’s buyback regime collapses → stock drops 20%+ → the whole house of cards comes down.

This is not hypothetical. In 2021, a fire at a Tokyo factory owned by Renesas Electronics—a much smaller chipmaker—disrupted global automotive production for months. Samsung’s HBM production is far more central to the AI supply chain than Renesas was to auto manufacturing. A two-week halt would ripple through every major AI server manufacturer worldwide. The fact that a single factory in Suwon is effectively a single point of failure for the entire AI trade is not as widely appreciated as it should be. And that is just the most acute vulnerability. More broadly, the AI buildout is hundreds of data centers competing for finite power, water, and land. When Nvidia published its Q1 earnings in April, the company also admitted it has ceded the Chinese market to Huawei. That is to say: China, which once accounted for at least one-fifth of Nvidia’s data-center revenue, stopped buying Nvidia’s best chips, because their own firms were told to buy local. The second-largest economy on earth is effectively building a parallel AI infrastructure without Nvidia, whose stock has now fallen after four consecutive perfect quarters—including this one—suggests the market may be beginning to sense this uncomfortable truth. Into this void step the only narrative strong enough to override and placate every macroeconomic anxiety: Artificial Intelligence. The market, however, is not trading AI as a sector, but rather as the central operating system of future corporate profitability. The monstrous capex of hyper-scalers—tech giants like Amazon, Microsoft, Google, Meta, Oracle, etc.—is no longer confined to semiconductors and chips but has spread to energy infrastructure, cooling systems, networking, data centers, cloud architectures, financing vehicles, industrial suppliers, software ecosystems. How long can this last hurrah of hyper-financialized capitalism continue? In South Korea, which is basically a massive microchip shaped like a nation, SK Hynix and Micron have each the $1 trillion threshold—with Micron adding $220 billion in a single day. South Korea’s KOSPI is officially up almost 100% in 2026. Semiconductors account of S&P 500 market cap: nearly one in five dollars.

The inevitable result of Trump’s tariff war will be a severe disruption to the global supply chain. As a nation who sits at the bottom end of the supply chain with its over consumption and reliance on imports for both consumer and business needs, such a disruption will lead to inflation and an economic recession. To counter higher inflation and economic downturn, the Fed will have to raise interest rate and the government will increase spending to stimulate the economy. As the US government spending already accounts for a quarter of GDP, higher interest payments and more expenditures will further increase deficit, forcing more debt borrowing and more deficits – a perfect vicious cycle. Washington is solving none of the structural issues facing the US – infrastructure, education, lack of manufacturing competitiveness, overburdened finance. With his insane tariffs, he is bifurcating the world into two camps – the high cost and high barrier US-led west and the low-cost low barrier China-led global south.

Another super-huge advantage China has over US finance is that its bonds are yielding around 2 %. Compare this to US bonds yielding 5%. Just this one factor alone will contain any inflation tendencies in China. In fact, China is experiencing deflation (prices of goods dropping), while inflation in the US and the west is climbing. The Federal Reserve is puffing its chest, trying to talk tough on rates. But it has a problem: oil. Crude is the one commodity that is both deeply financialized and fiercely industrial. It is the bridge between Wall Street and Main Street. So now the central bank is signaling hikes, and the market is pricing them in. But if oil spikes hard enough on the back of a confirmed and continued Hormuz closure, the economy will buckle, and the Fed will have no choice but to pivot fast. That means the hawkish rhetoric is vulnerable to a single and highly manipulable variable: crude. The real game is about the survival of an over-leveraged, hyper-financialized economy. And survival, in this context, requires lower rates. The game is far from over. It has not even reached its most “interesting” chapter. And now the final act might be unfolding faster than anyone expected.

The Damage Is Already Done

Forget the tit-for-tat strikes. The real story is that the global supply chains that keep the world fed and fueled are already broken. And the closure of the Strait of Hormuz was the convenient justification for a structural crack that was always opening under our feet. The West’s economic model—based on abundant credit and the assumption of perpetual financial growth—is in terminal decline, and missile strikes are supposed to throw smoke into the world’s eyes over this elementary truth. The war, then, is not the cause; it is controlled demolition, always flirting with getting out of control. While on the one hand it provides immediate profit gratification through market manipulation, on the other it tells us that the system is running out of road and accelerating down its destructive path. So, what’s next? The Fed’s chest-puffing about rate hikes and the hawkish rhetoric won’t survive long, because a recession is already locked in. Broken supply chains + higher energy and food cost (US inflation at 10 % plus, i.e., declining US dollar purchasing power) + cratering jobs and consumer = severe economic contraction. And contraction requires one thing from the central banks: cheap dollars.

The Gold and Metals Selloff: A Sign of Desperation

This is where the picture becomes even clearer. Gold and silver have been selling off sharply. On the surface, this looks like a paradox: geopolitical chaos and inflation should send precious metals higher. But rather than a rejection of their safe-haven status, the selloff is a desperate cover against margin calls. When leveraged positions start to unravel—whether in equities, derivatives, or commodities—institutions and hedge funds need cash fast. And the most liquid assets they hold are gold, silver, and other highly traded metals. This is therefore the signature of a system under extreme stress: fire sales of the most liquid assets to cover margin calls elsewhere. All this while the People’s Bank of China (PBoC) its official gold reserves by 9.95 tons in May, marking its nineteenth consecutive month of accumulation. While Western institutions are selling gold to survive, the East is buying it to prepare. It is the same dynamic we saw in March 2020, when gold sold off even as the world was collapsing. It was not a sign that gold had lost its value but that the financialized system was cannibalizing its own safe havens to survive the next hour. Investors and leveraged funds liquidated highly liquid assets like gold, which dropped 10% to 15%, to raise cash, cover heavy losses in other asset classes, and meet the dreaded margin calls. So, let’s keep this firmly in mind when we watch the news. What we are witnessing is a civilizational event, not a cyclical downturn.

· Oil—the lifeblood of the modern economy—is in structural shortage.

· Fertilizers—the basis of global food production—are being choked off.

· Debt—the foundation of “Western prosperity”—is at levels that can never be repaid without inflation or default.

· Liquidity is drying out (excess liquidity now turning for the first time since 2021).

· Trust—the invisible glue of the financial system—is evaporating.

Glass-Steagall De-Dollarization

This fact is known to everyone around the world with eyes open enough to see, and who cares enough to see. Country after country is recognizing it, and what’s going on is a process of de-dollarization—people saying, “We see that the Titanic is sinking. We don’t want to go down with it.” This is happening for three reasons. First of all, they see that the Titanic is going under, and they don’t want to stay on board. Secondly, they see that the sanctions applied to Russia did not destroy Russia. As a top Brazilian official stated recently, “Who’s afraid of the big bad wolf?” on this question of dealing with China and so on. Russia didn’t go under; in fact, even the SWIFT nuclear option, of removing Russia from the SWIFT [banking communications] system failed to have an effect, as had been forecast it would. But the other thing that’s going on, is that there is some leadership. There’s leadership among nations: You have the ideas being presented by Xi Jinping, by Putin, by leaders in Brazil, Saudi Arabia, Türkiye, Indonesia, and others, that are clearly pointing in the direction of increasing the role of local currencies, non-dollar currencies. First through swaps—bank-to-bank swaps to have credit lines; second, through trade denominated, for example, in yuan. And then to actually set up full-scale clearinghouse operations which will permit not only trade, but investment in the respective economies. The Chinese Yuan Is Becoming a Global Currency

Now, if you take a look at the map above, you will see that a quick approximation of the number of countries involved in this, using the yuan in one way or another, is over 30, and it’s well over half the population of the planet in point of fact. So, this is the process that is going on, and it is spreading very rapidly. Now, many people in the United States have gotten on their high horse and said, “This is terrible, this is an attack on us. This is getting rid of the dollar; you’re attacking us. We’ve got to stop this. Chinas got to be stopped; Russia’s got to be stopped; Iran’s got to be stopped; Brazil’s got to be stopped; they’ve all got to be stopped.” Well, this is nonsense, because the fact of the matter is that the United States should also de-dollarize. The dollar is a cancerous, speculative animal that has taken over the US financial system. And it has put the world under the control of the City of London and Wall Street. That process in the United States has a very specific name and history. It’s called the Glass-Steagall principle. Because the Glass-Steagall principle is nothing but de-Wall Street-dollarization; it’s a full separation from the speculative dollar under the control of the City of London and Wall Street.

Conclusion

Both wars – Ukraine and Gaza/Iran was meant to break up Russia and Iran. There were many geopolitical advantages to do so for the Rockefellers. But the key reason was to prolong the life of the Petro-dollar. Both Russia and Iran are oil exporters, who are now selling their product for anything but the dollar. The US attempts failed in both cases. Nations, companies and individuals are fleeing from the dollar. Globalization reduced inflation in the West and increased inflation in the Global South. Today, globalization is receding, de-dollarization is increasing, and as it does, inflation is rising in the West. New York and the Rockefellers have prepared an off-ramp, or back-up plan to save their Empire. Use external crisis as an excuse to implement ICE NINE, or parts of it, and use AI as a surveillance and control technique to force people to follow their rules. In short, an electronic prison. Our next article is called “The RUSSIA/IRAN/CHINA Triangle “